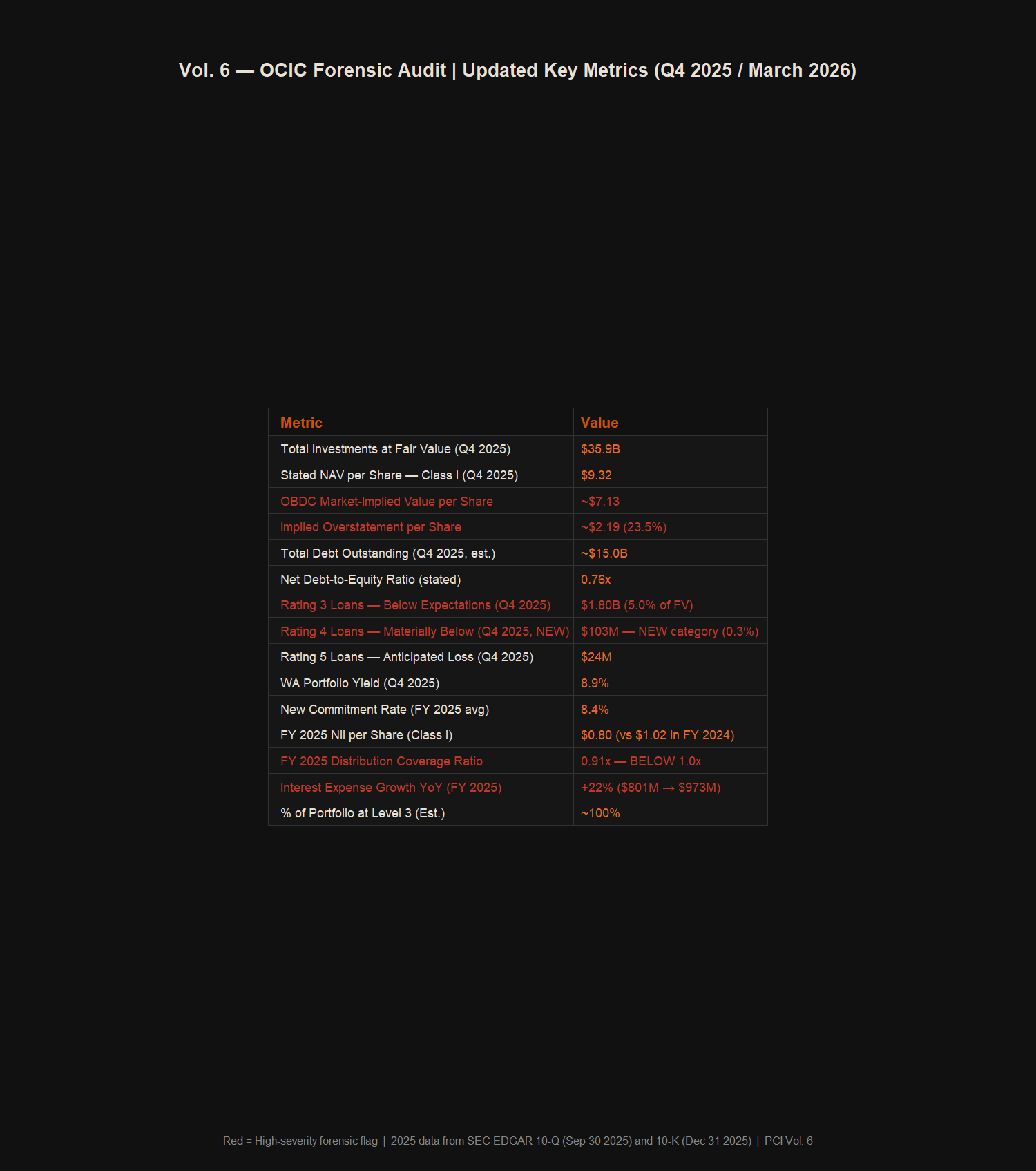

Vol. 6 — Forensic Audit: Blue Owl Credit Income Corp

The Buried Deterioration

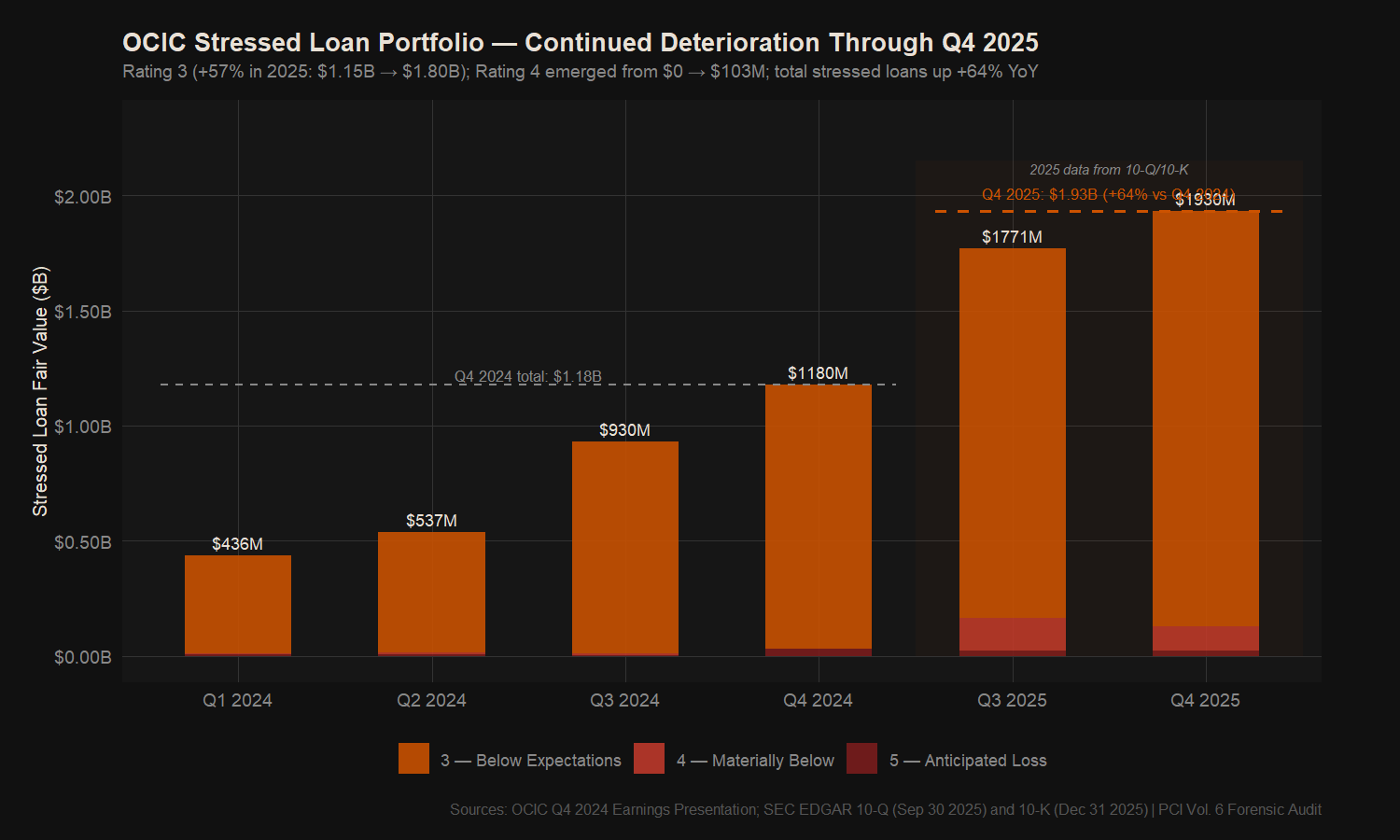

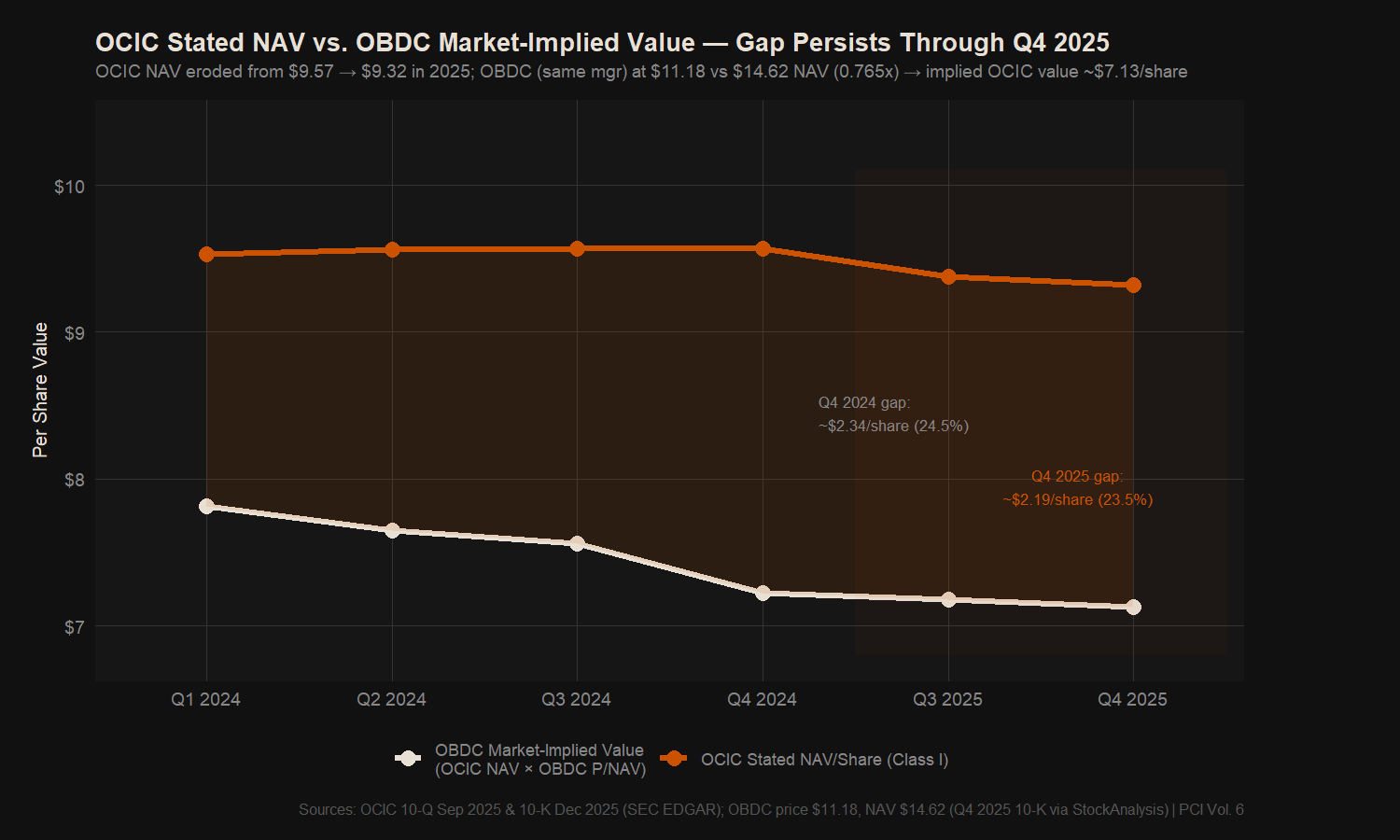

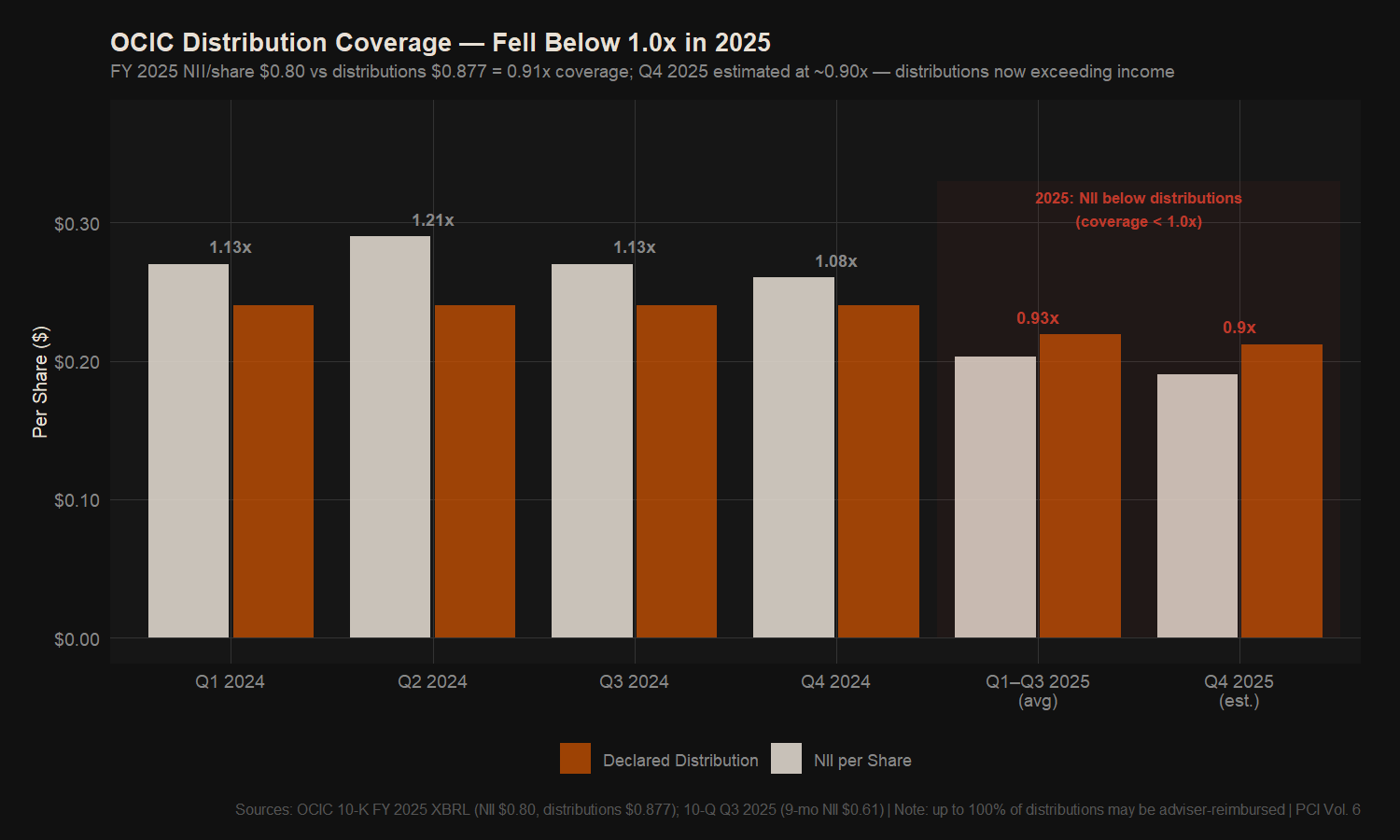

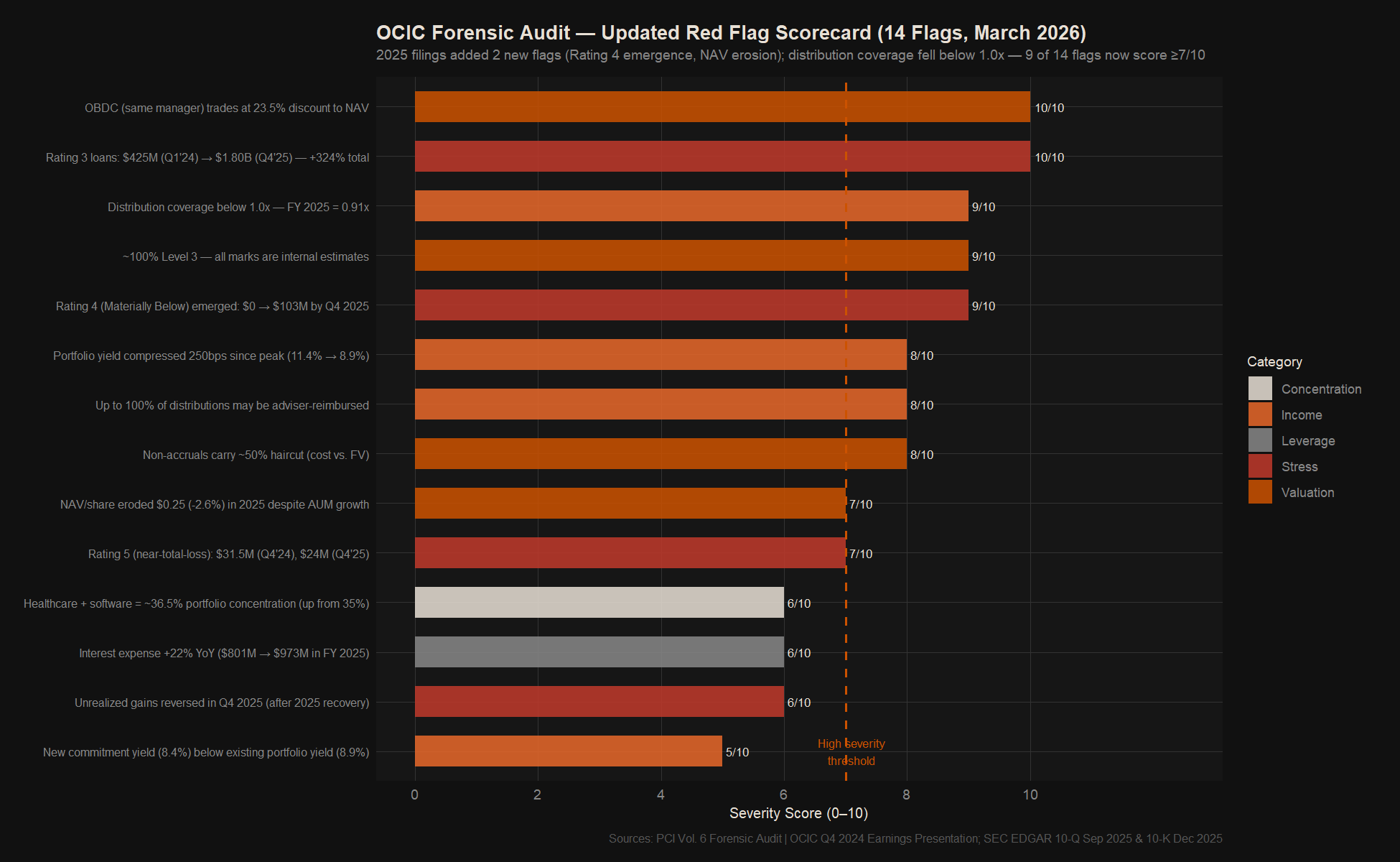

OCIC's headline NAV has been managed to near-flatness — $9.53 to $9.57 across all of 2024, then $9.32 by Q4 2025. But the internal portfolio rating data tells a different story. Rating 3 (Below Expectations) loans have grown +324% from Q1 2024 to Q4 2025 ($425M → $1.80B). Rating 4 (Materially Below) — a category that did not exist in Q4 2024 — emerged at $103M by year-end 2025. FY 2025 NII per share fell to $0.80 versus distributions of $0.877 — distribution coverage fell below 1.0× for the first time. And the publicly traded vehicle run by the same manager — OBDC — continues to trade at a ~23.5% discount to its own stated NAV. Applied to OCIC, that implies a market-clearing value of approximately $7.13 per share against the stated $9.32.

Internal Rating Migration — Updated Through Q4 2025 (+324% Total Stressed Growth)

Distribution Coverage — Fell Below 1.0× in FY 2025

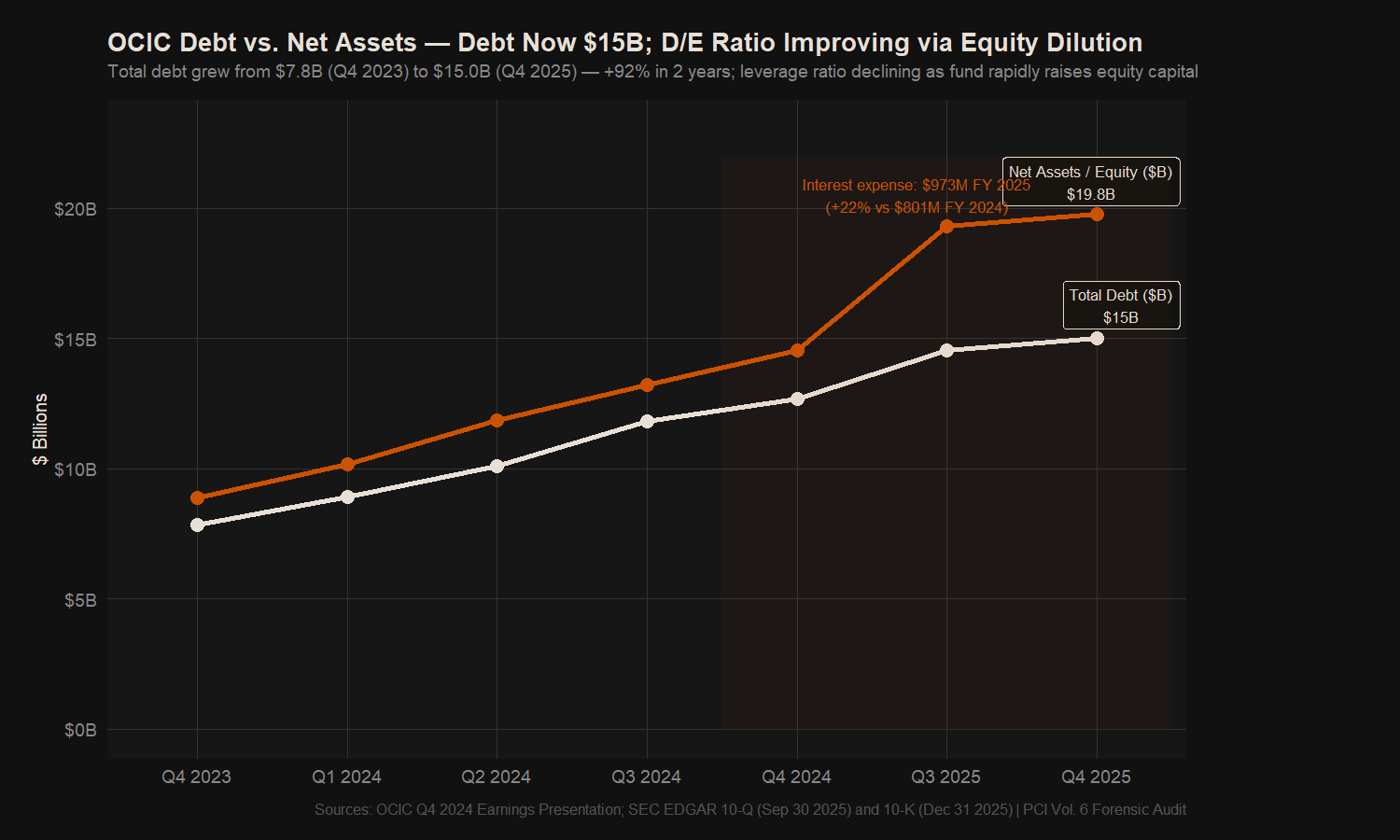

Debt Growth — $7.8B to $15.0B in Two Years; Interest Expense +22% in 2025

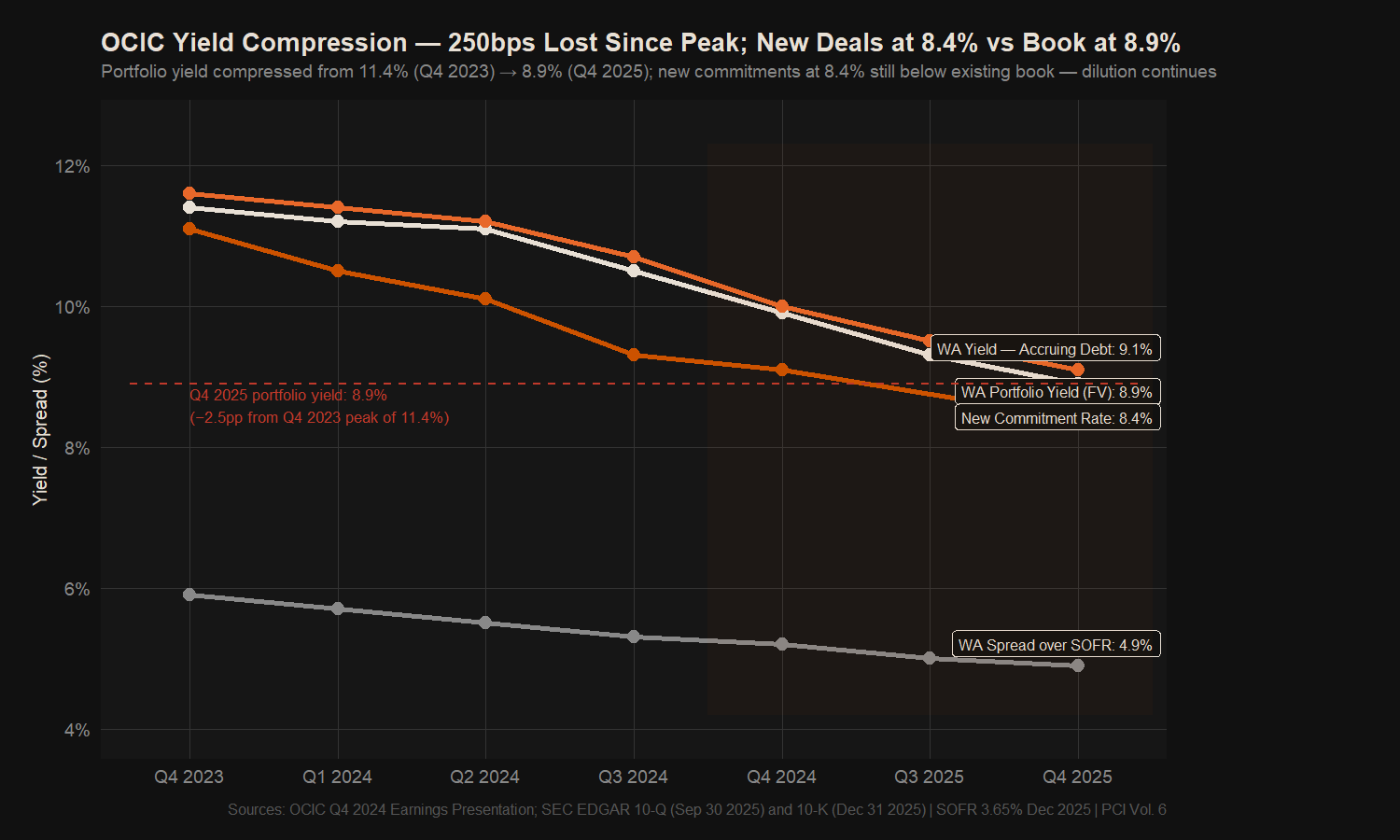

Yield Compression — 250bps Lost Since Peak; New Deals Still Below Book Yield

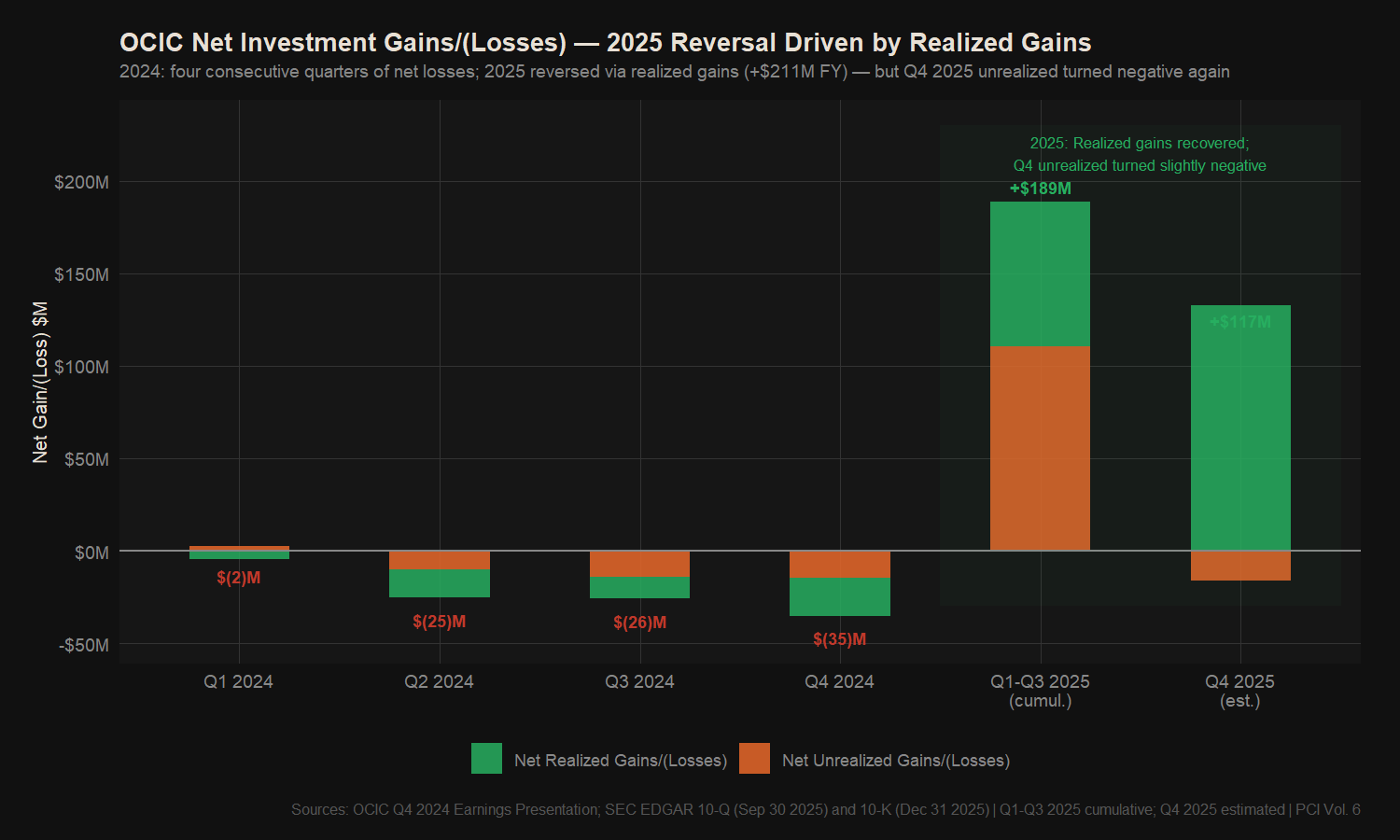

Investment Gains/(Losses) — 2025 Reversal via Realized Gains; Q4 Unrealized Negative Again

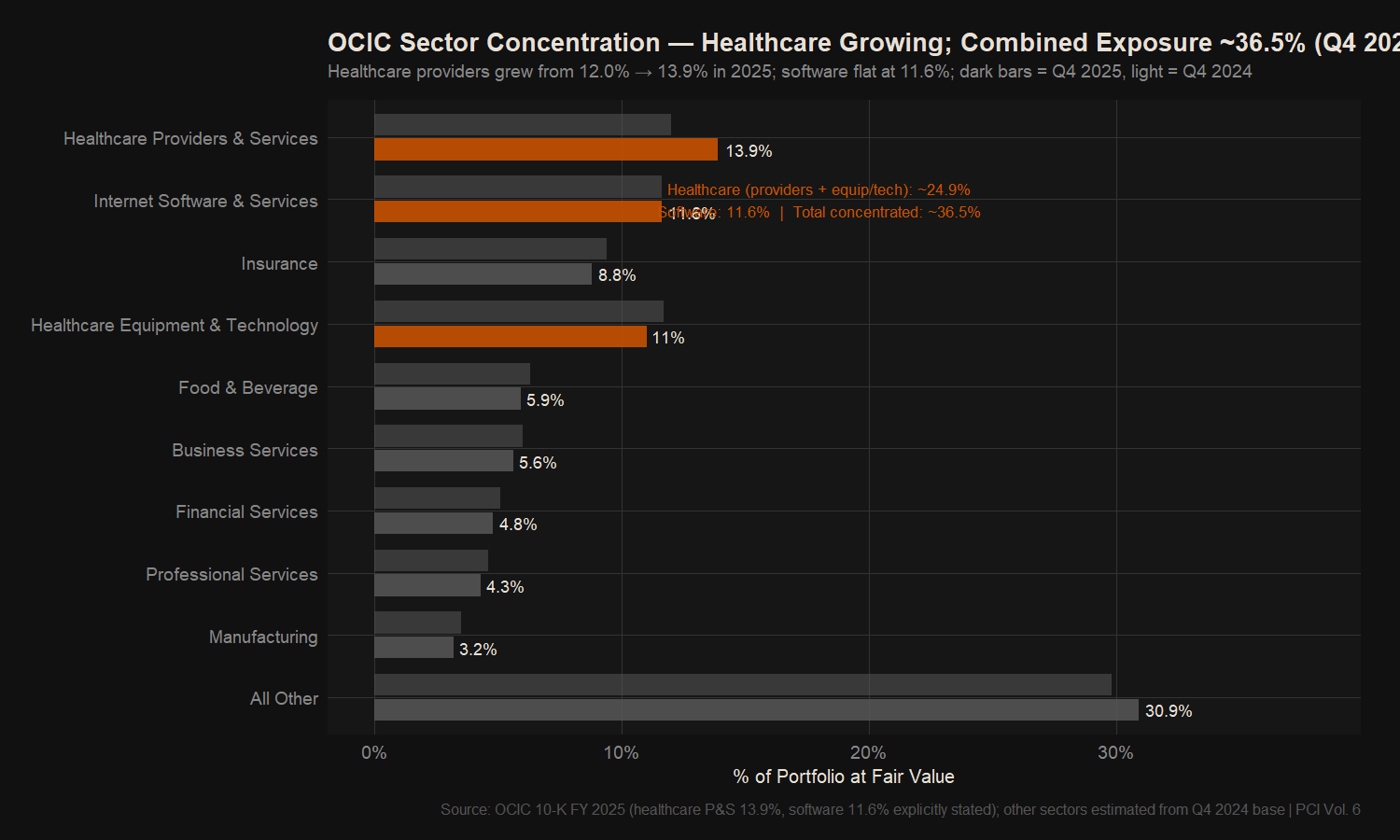

Sector Concentration — Healthcare Growing to 13.9%; Combined ~36.5%

Forensic Red Flag Scorecard — Updated: 14 Flags, 9 Scoring ≥7/10

Forensic Audit Summary Dashboard — Updated Q4 2025