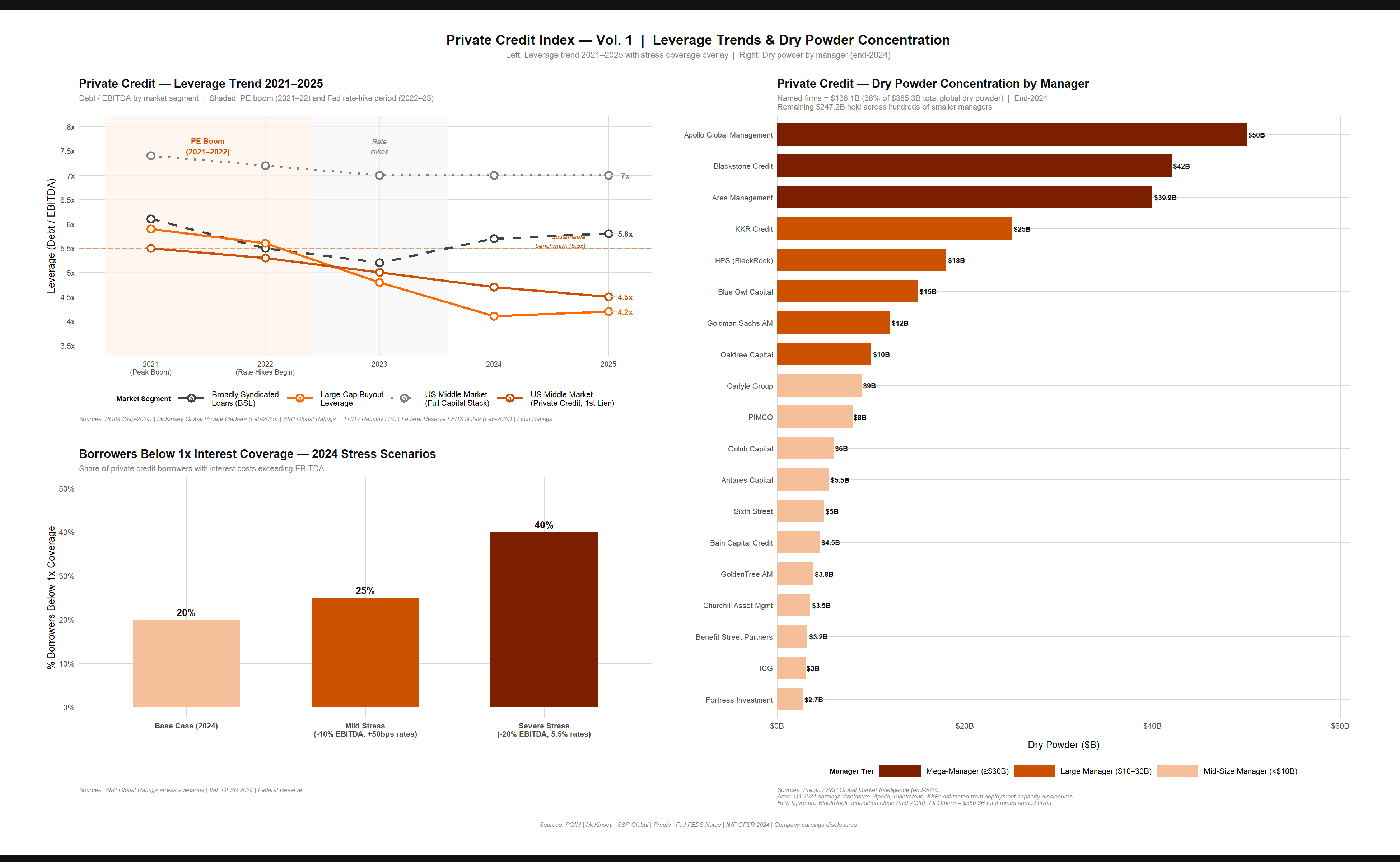

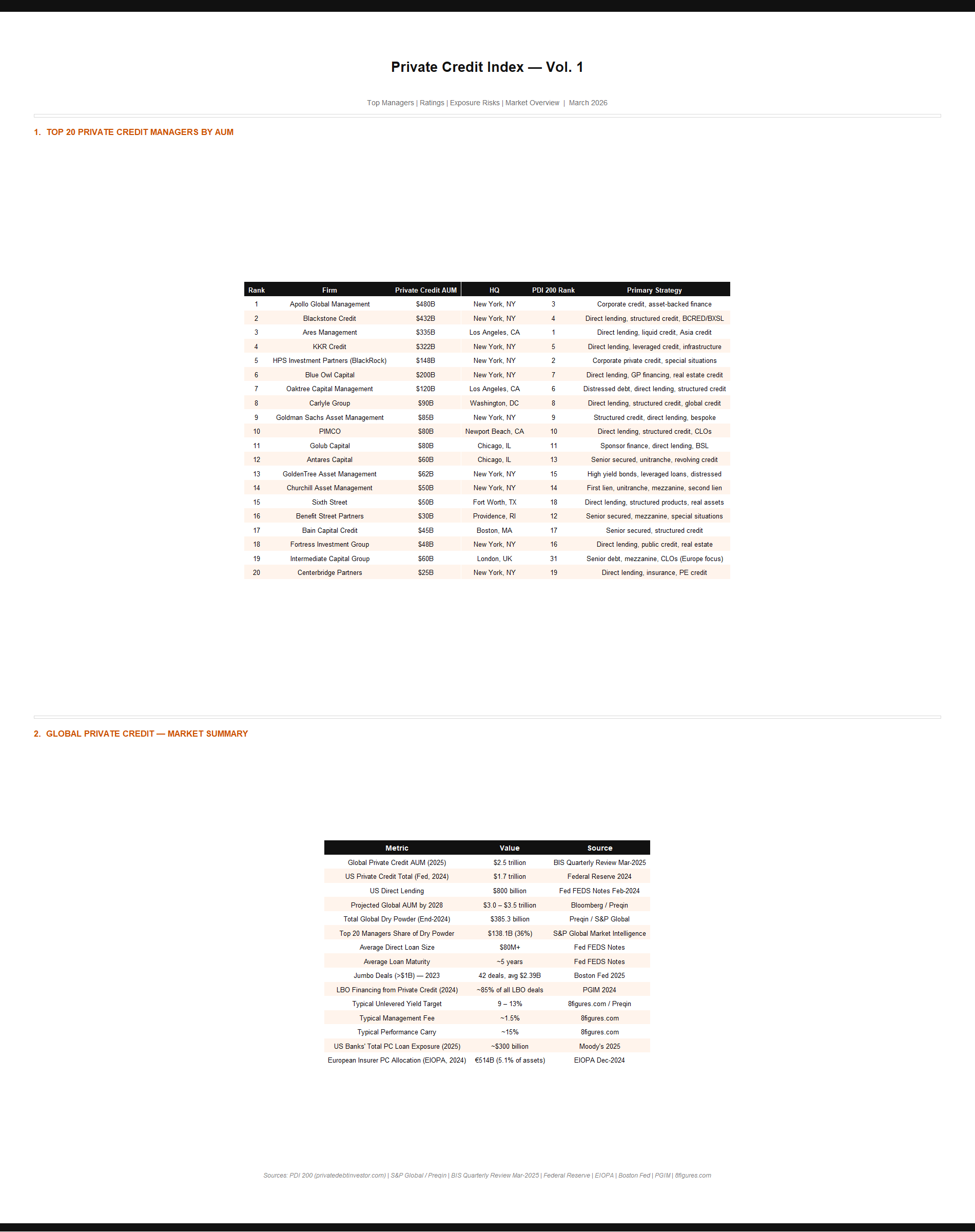

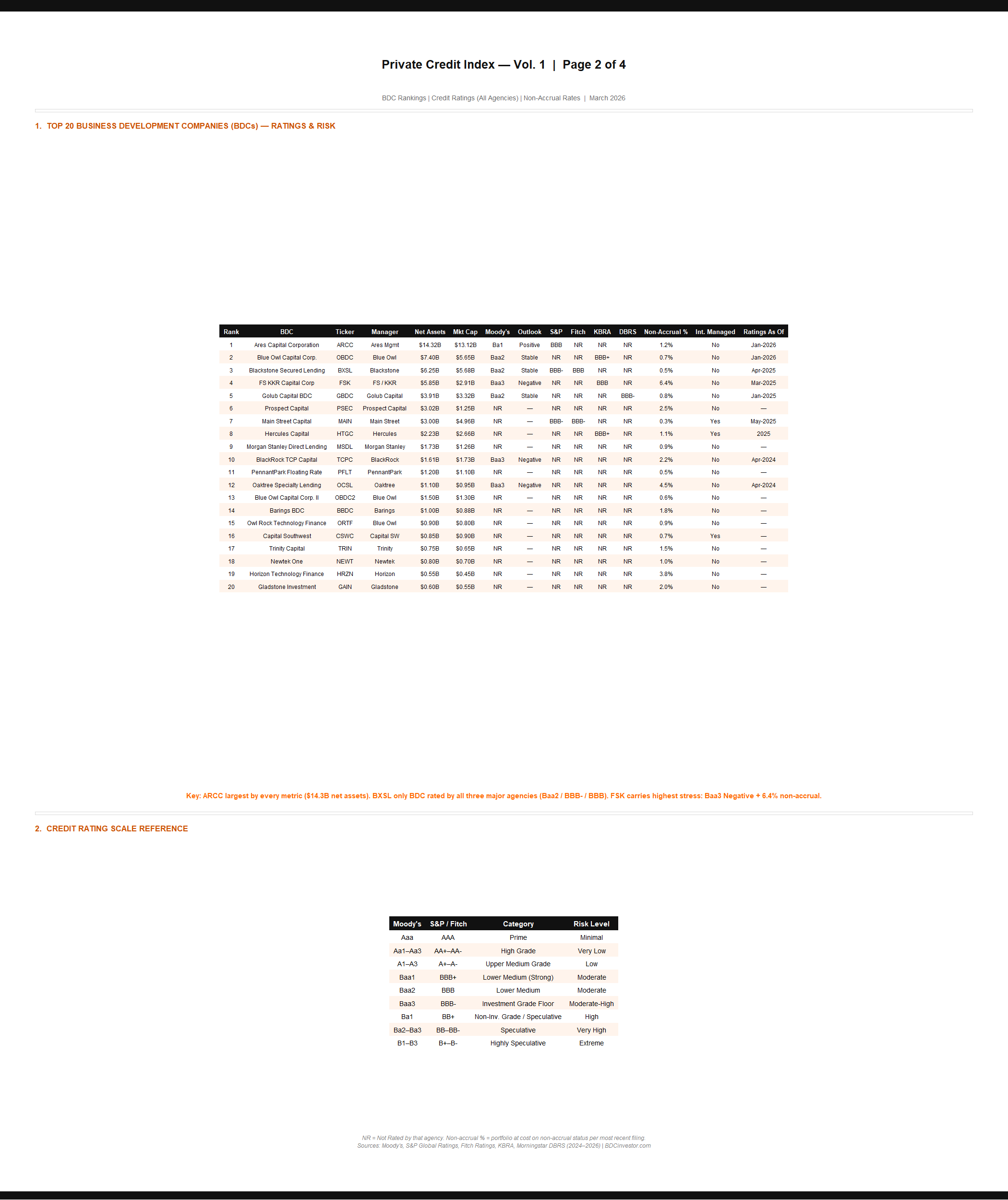

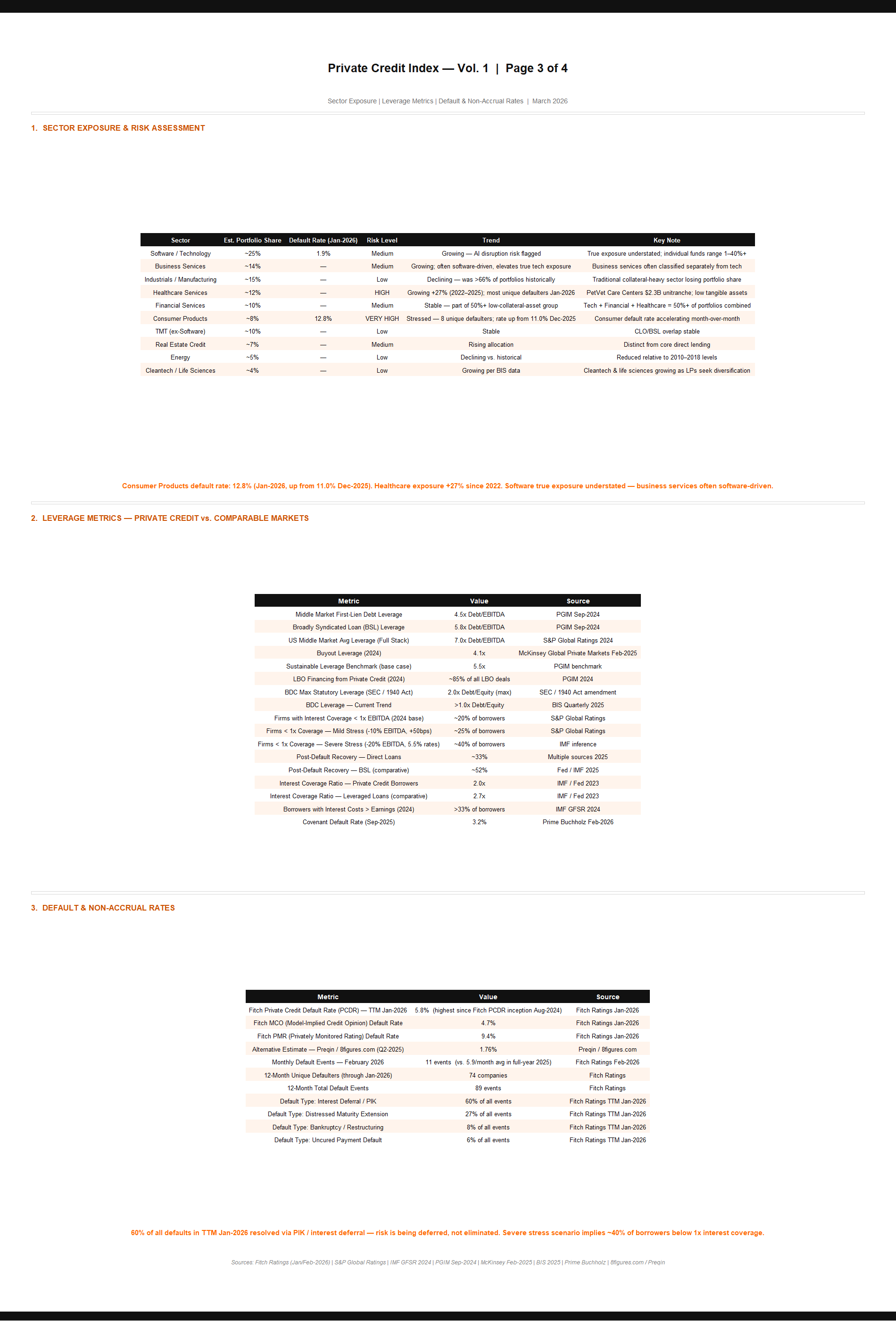

Vol. 1 — Full Static Exports

Index Tables, Heatmaps & Charts

High-resolution PNG exports from the R pipeline. Click any image to open full-screen.

Index Tables

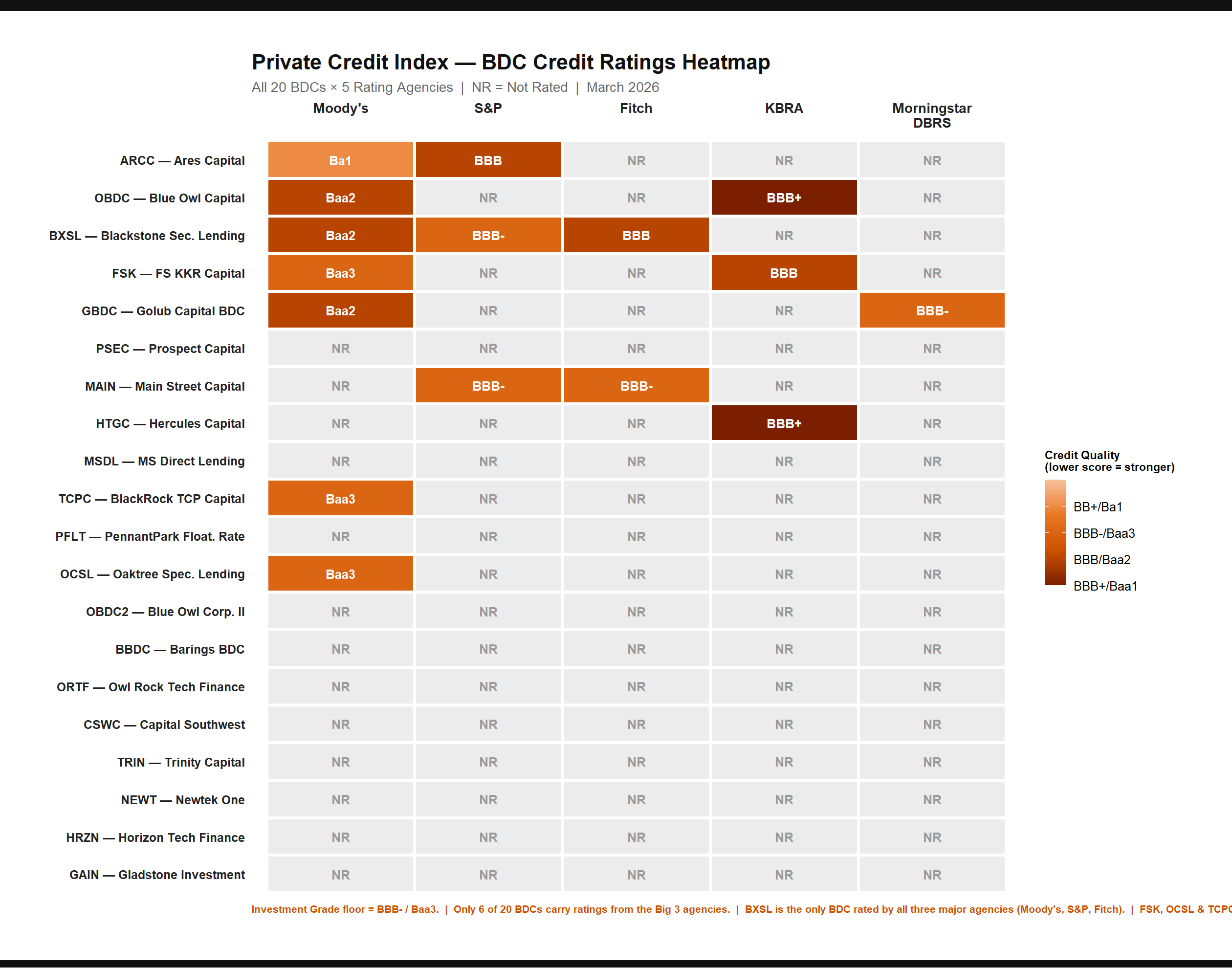

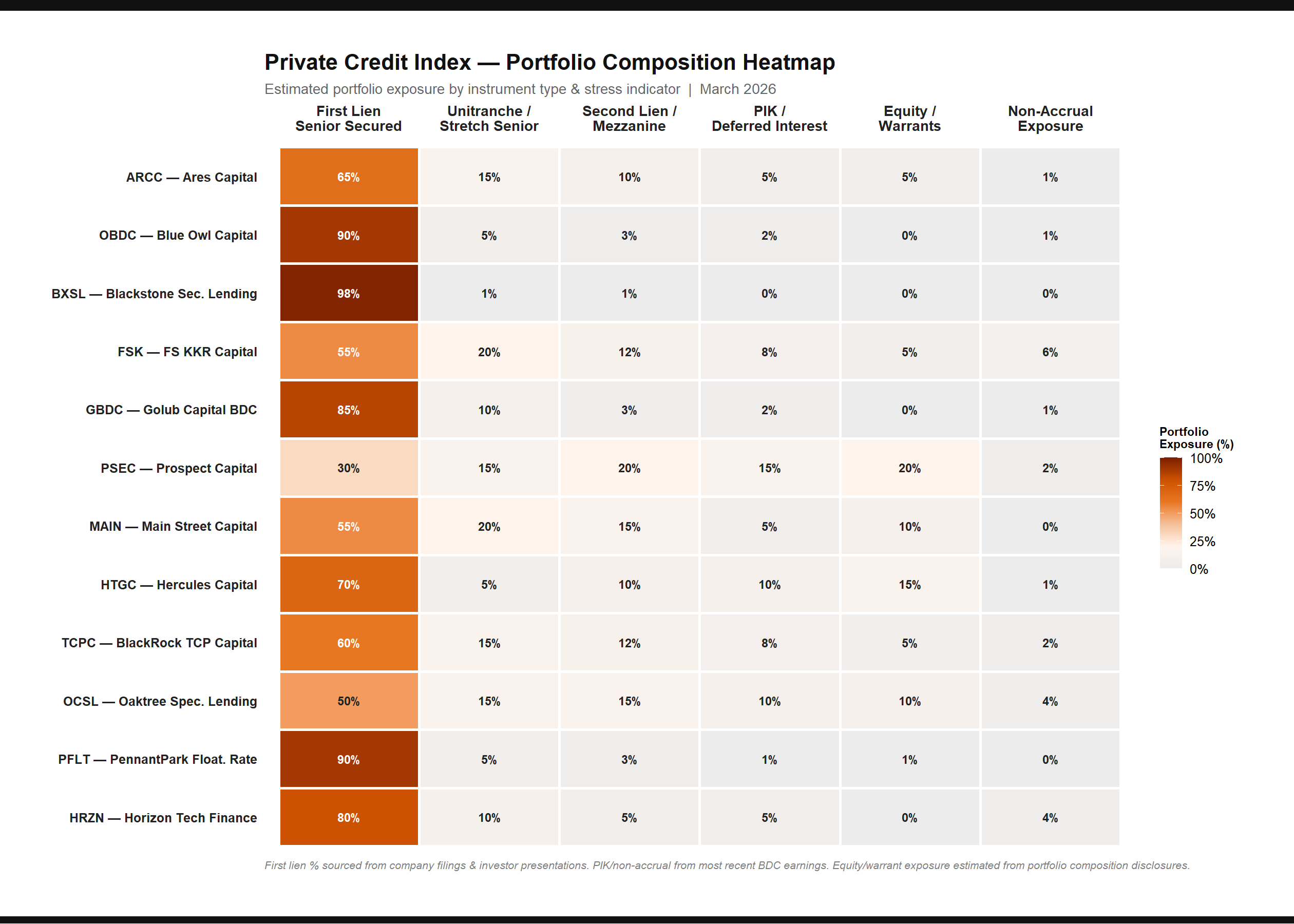

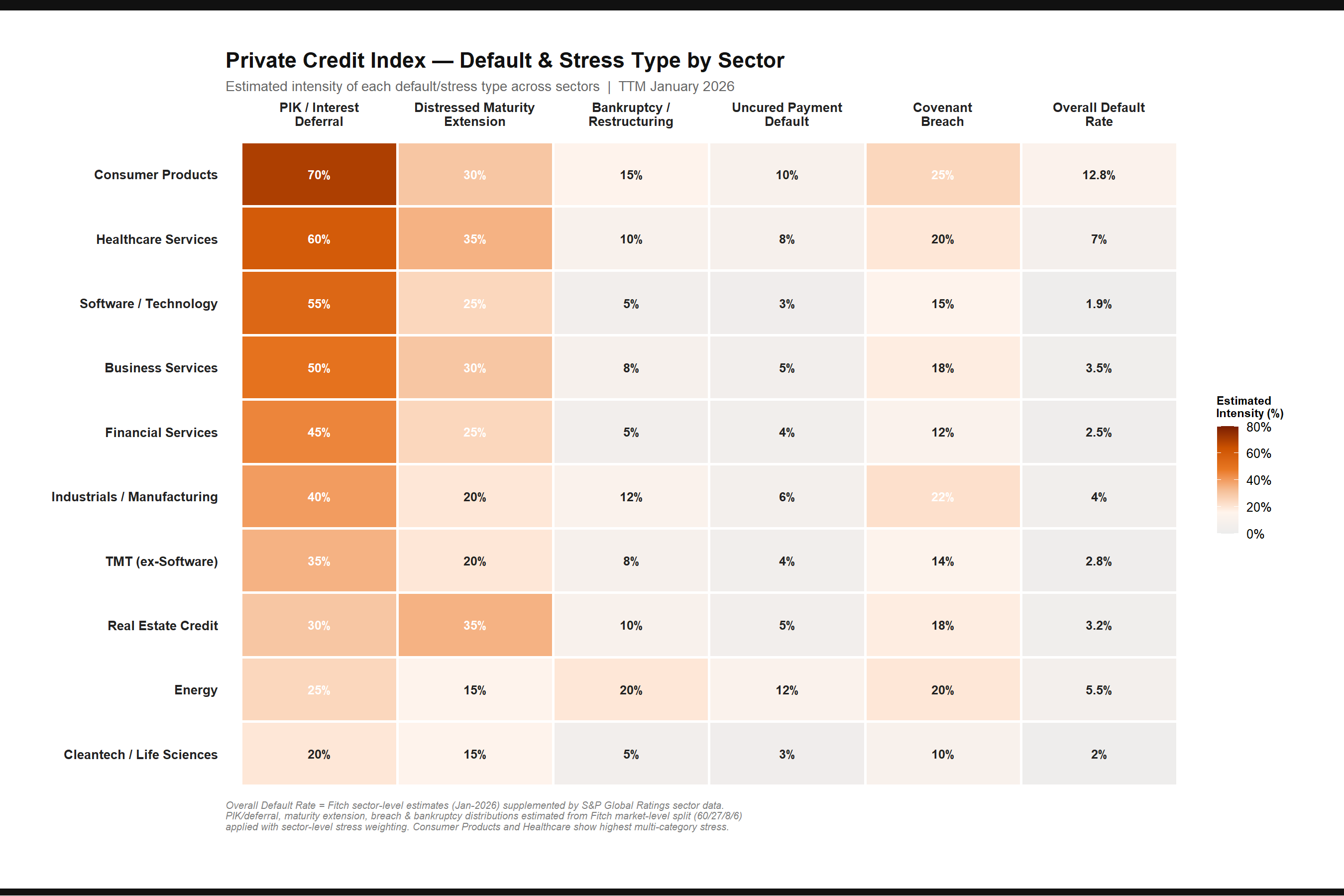

Heatmaps

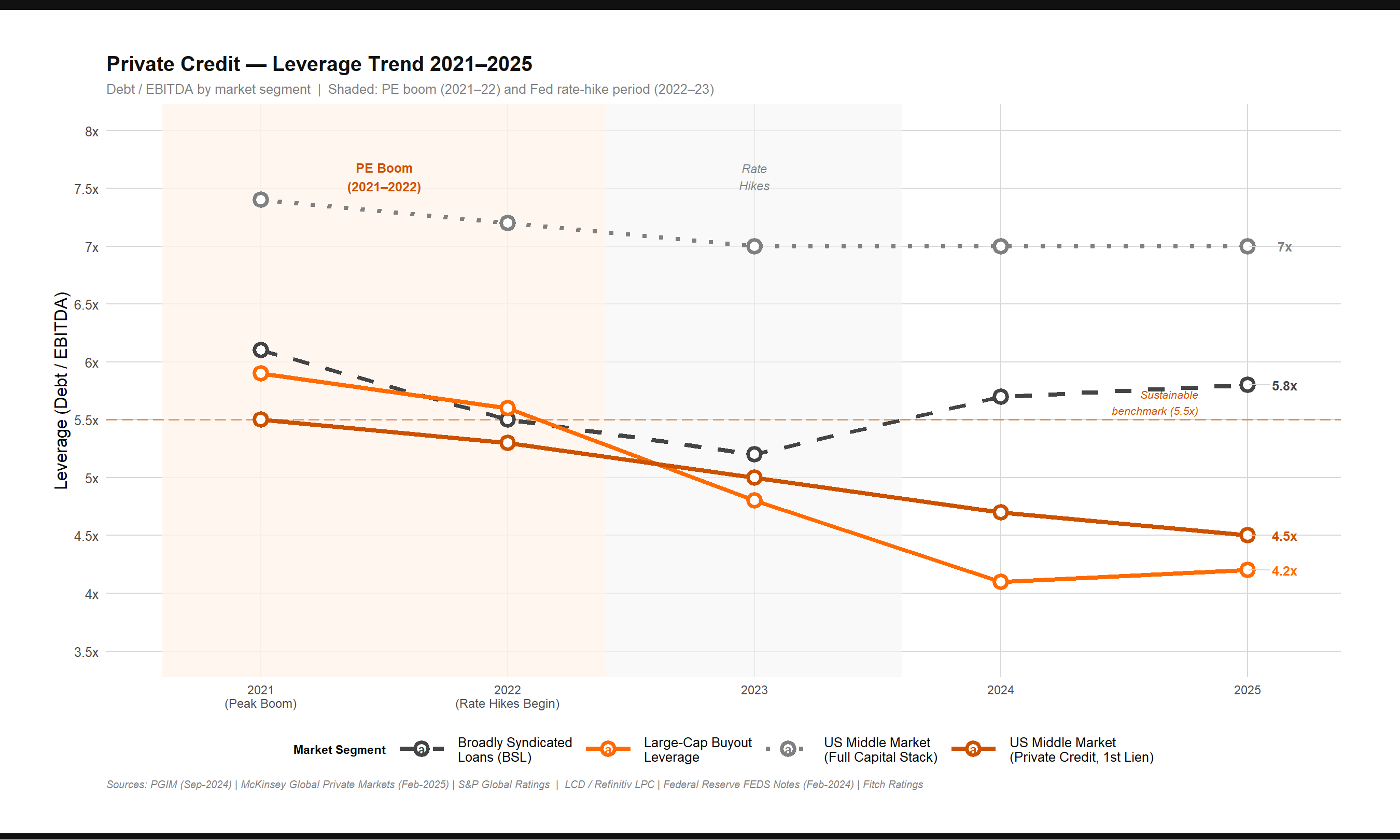

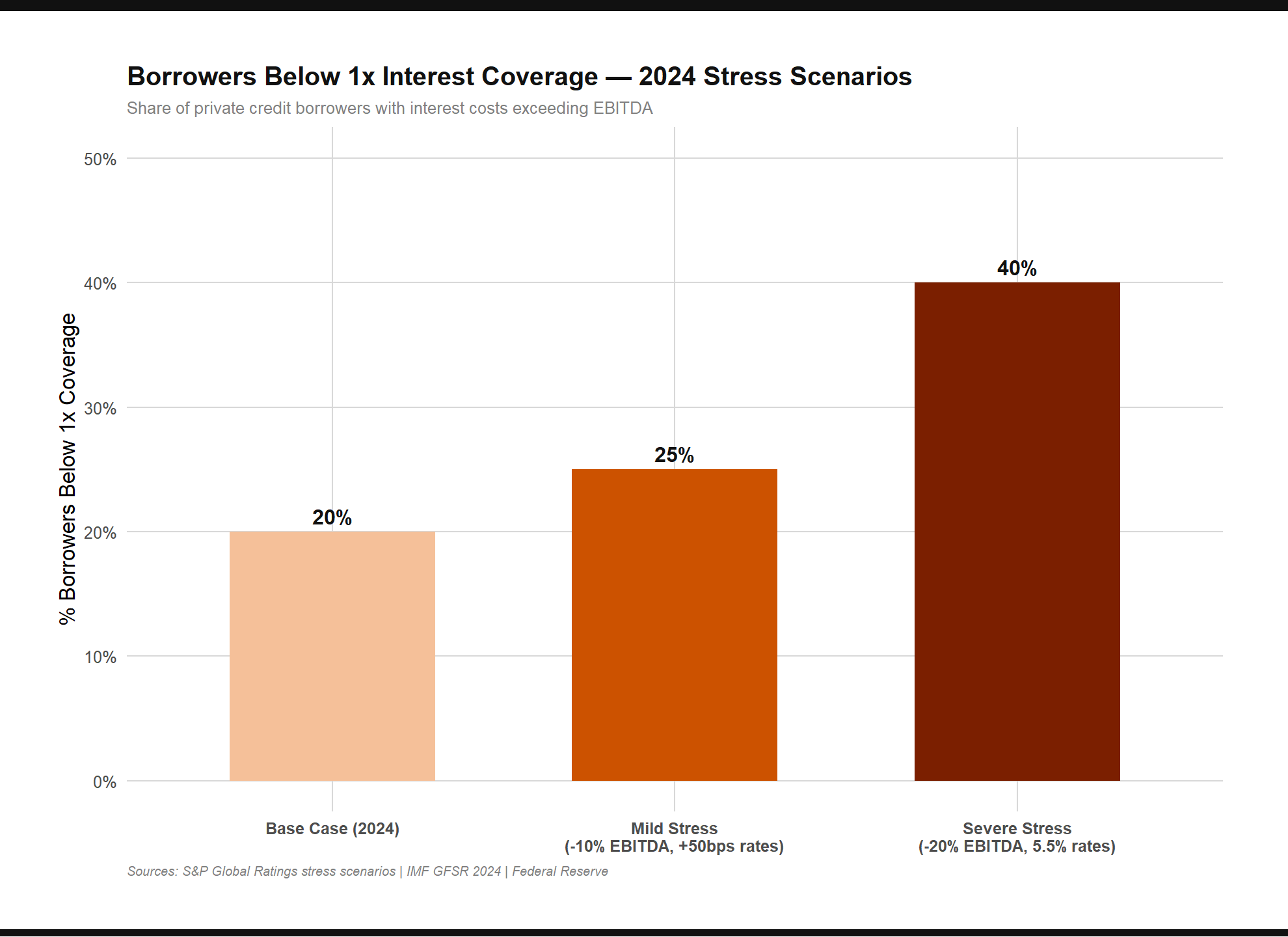

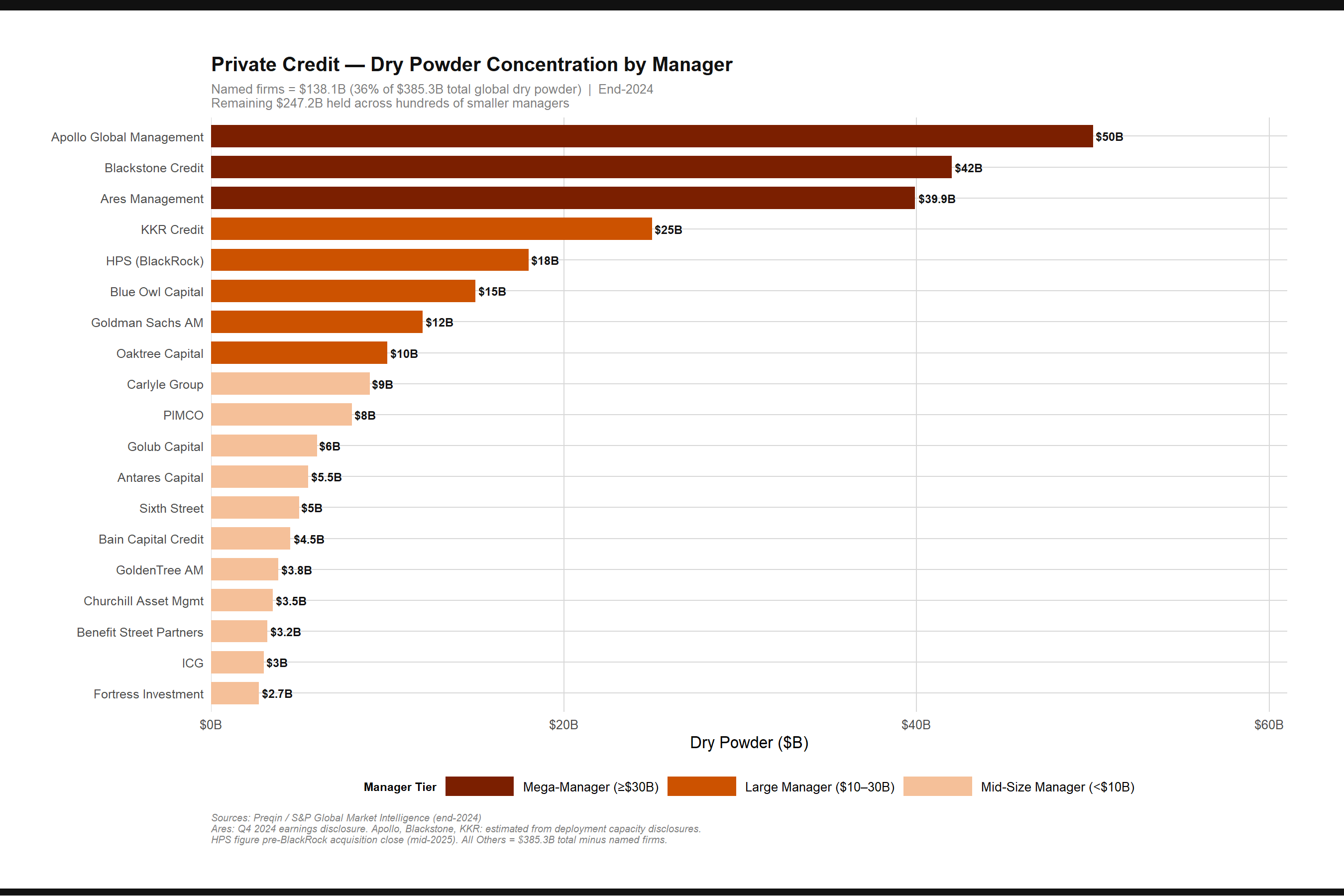

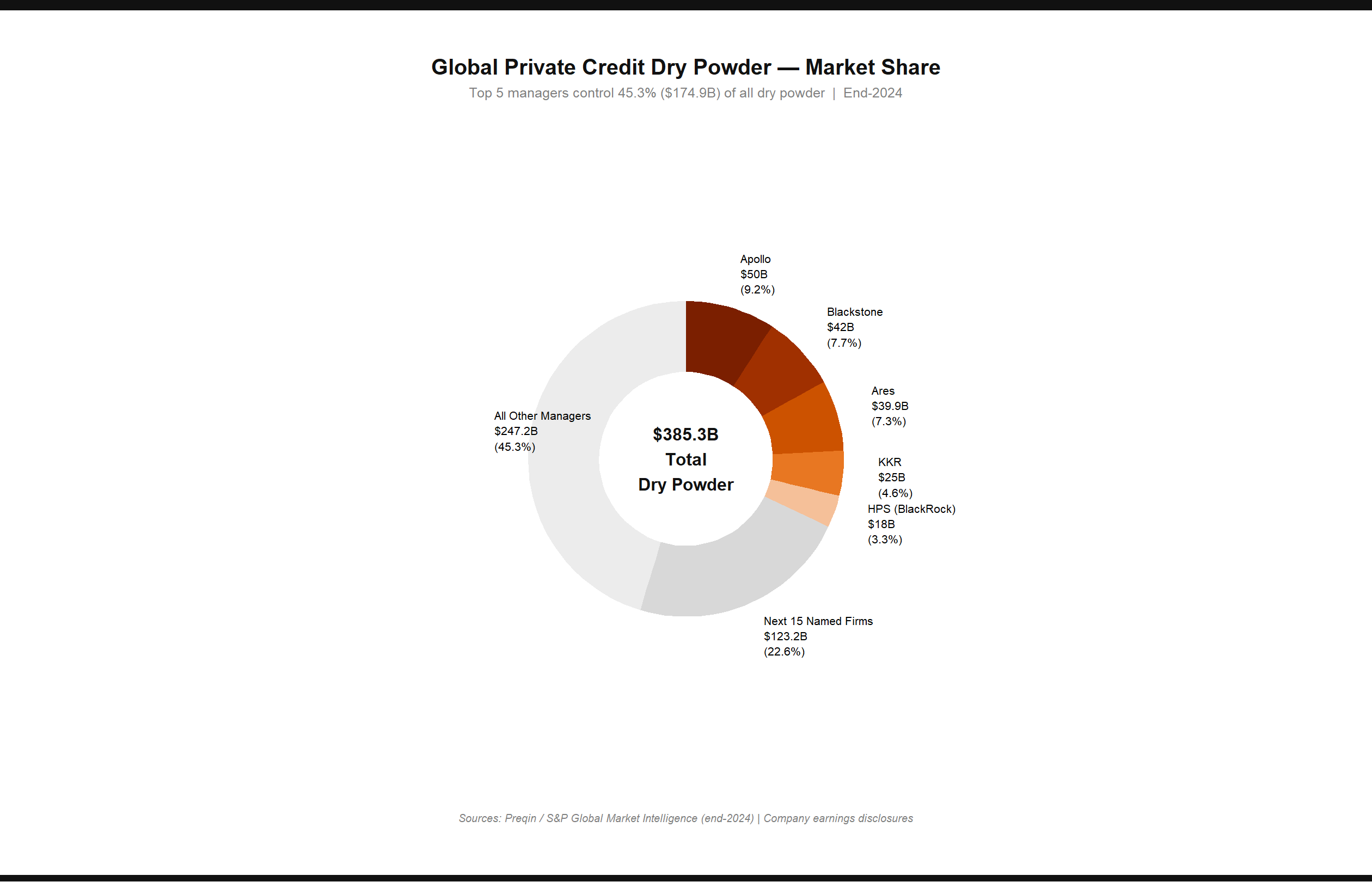

Leverage & Dry Powder