Vol. 4 — Market Structure Deep-Dive

Structural Forces Reshaping Private Credit

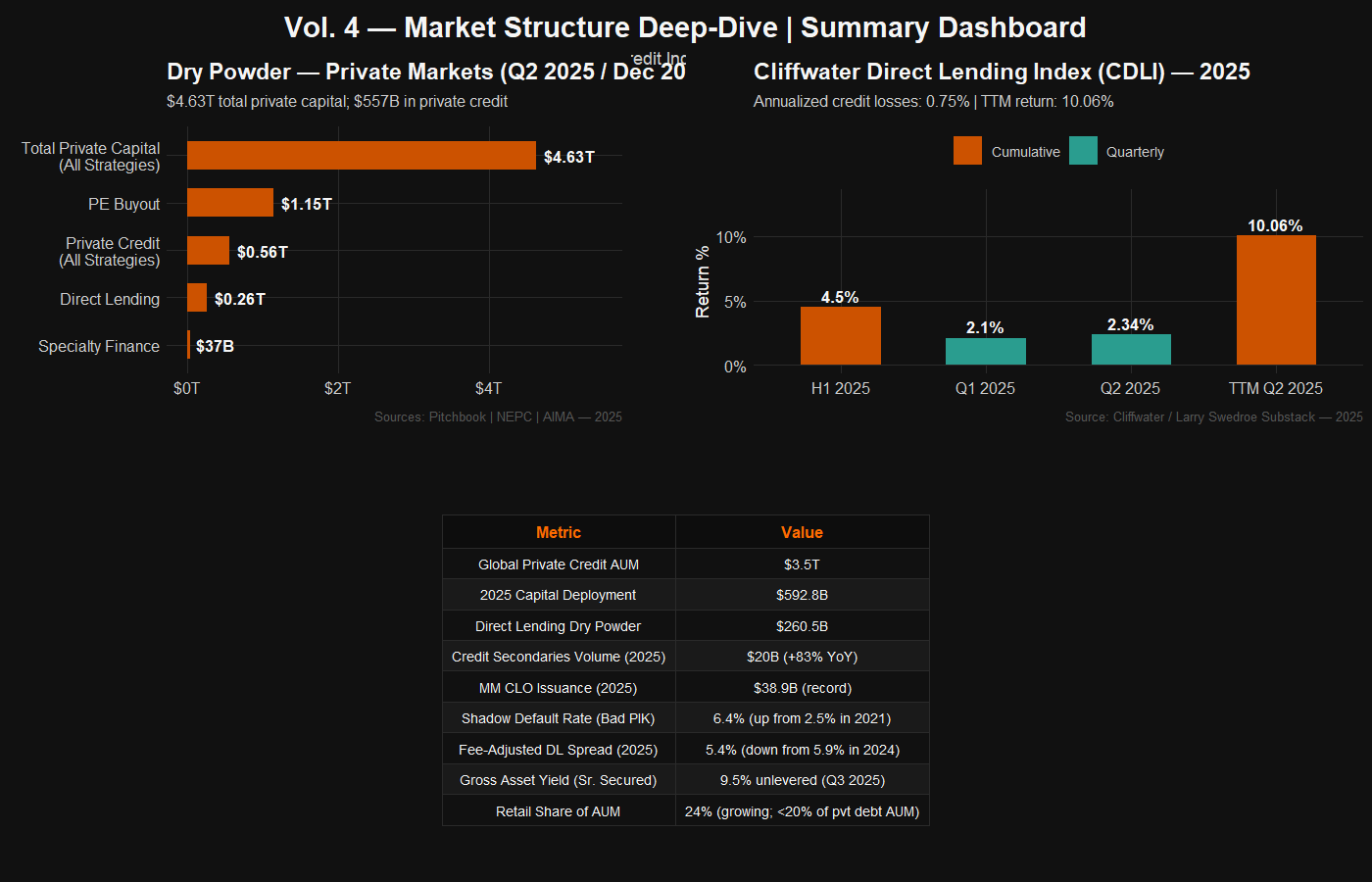

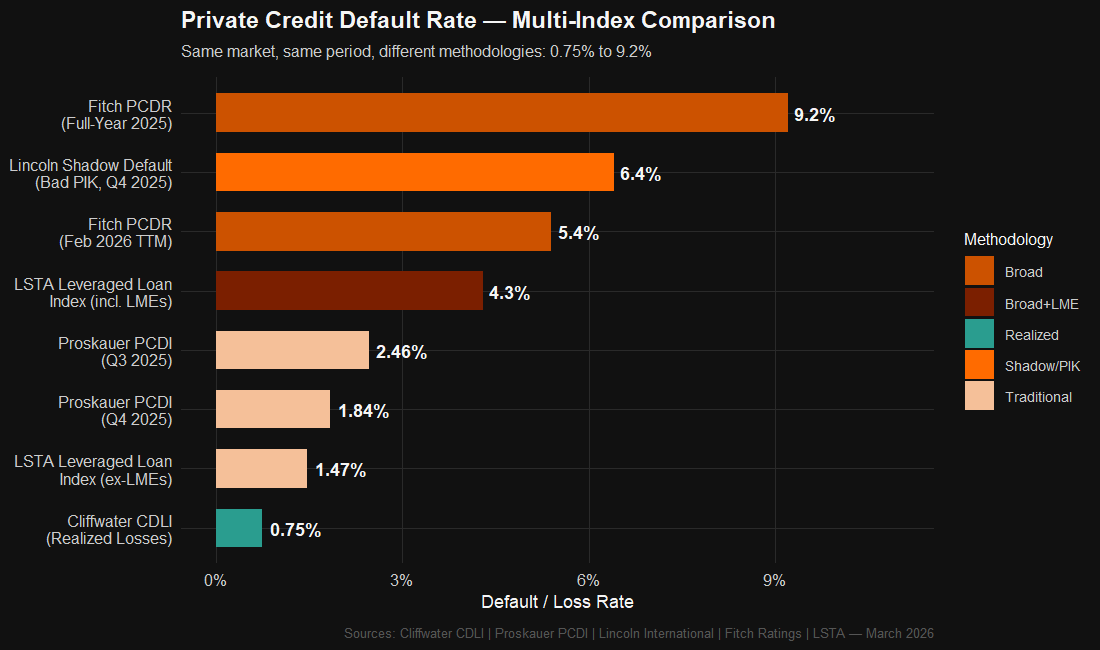

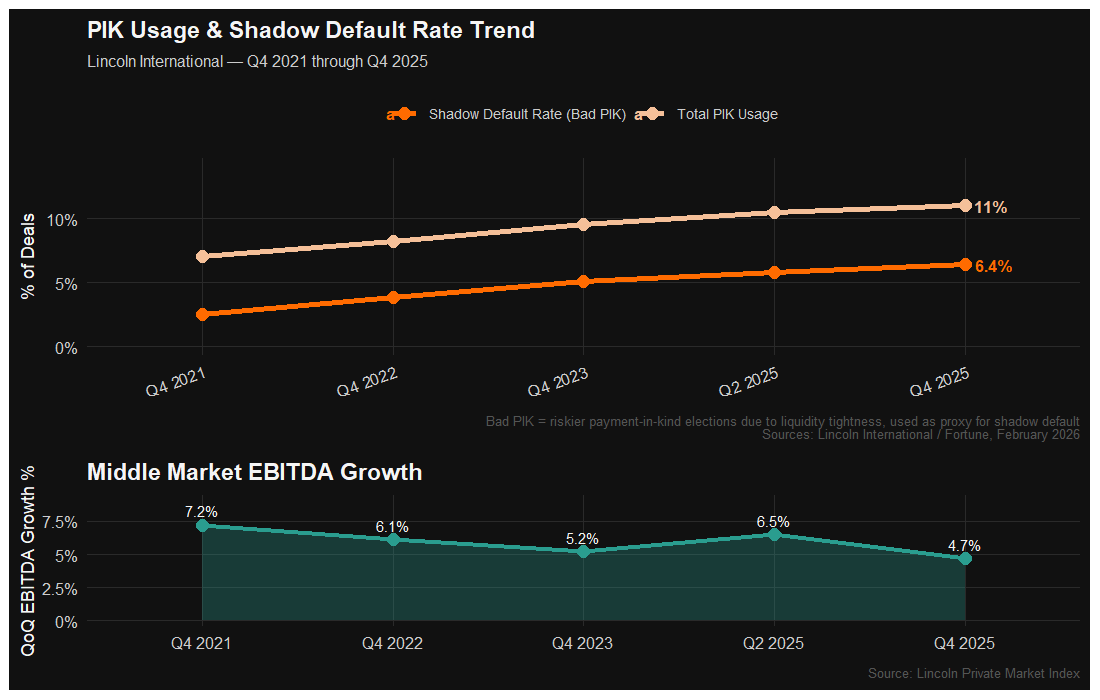

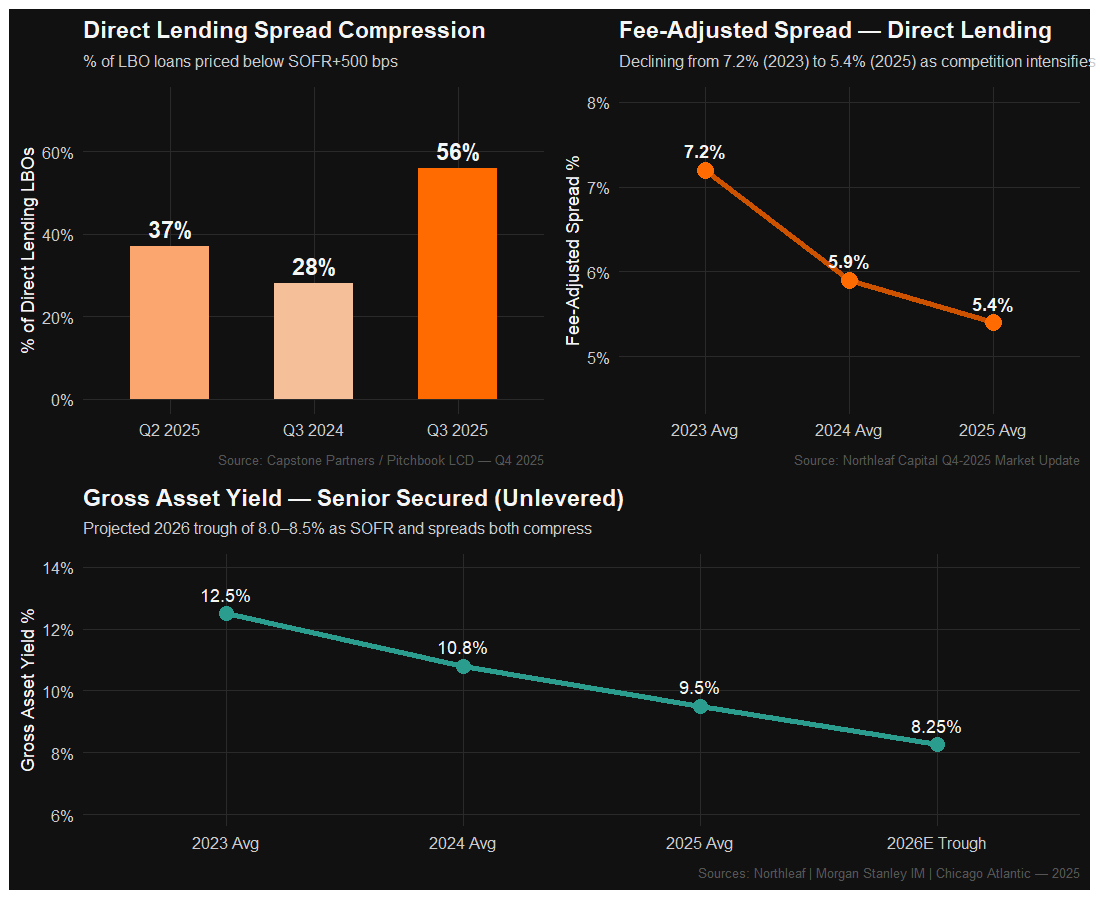

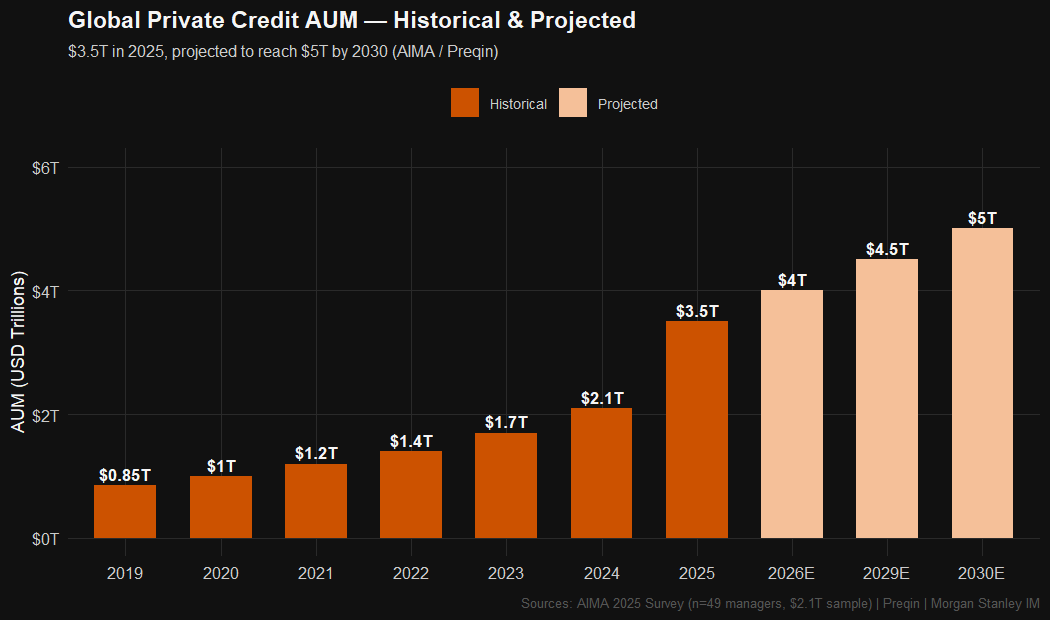

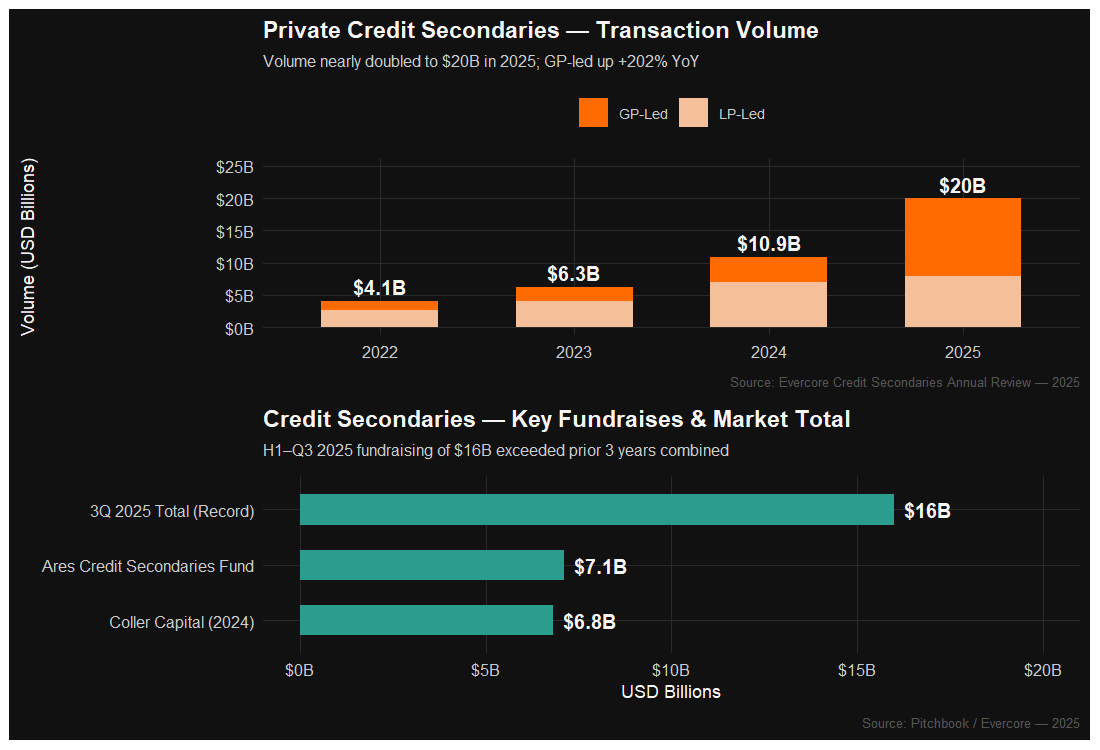

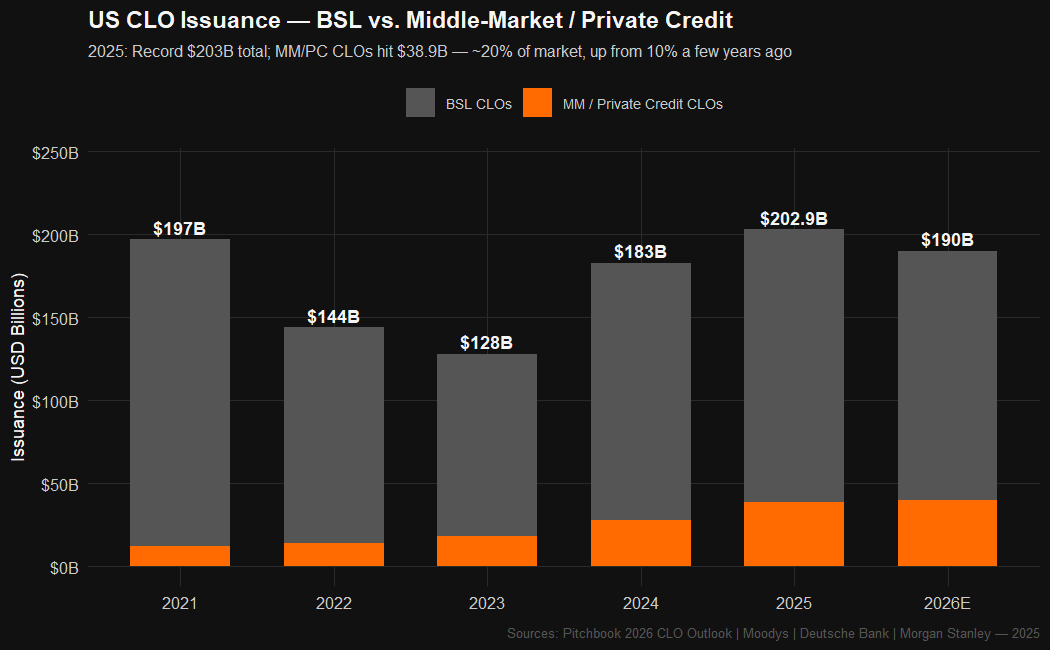

The same private credit market produces default rate readings of 0.75% (realized losses, CDLI) to 9.2% (Fitch full-year 2025) depending on methodology — a 12x range that reflects deep definitional opacity. Lincoln's shadow default rate (bad PIK) has more than doubled from 2.5% (Q4 2021) to 6.4% (Q4 2025), while direct lending spreads compressed over 160 bps since 2023. Global AUM reached $3.5T in 2025 — double the commonly cited $1.7T figure — with $592.8B deployed in 2024 alone. Credit secondaries nearly doubled to $20B, and MM CLO issuance hit a record $38.9B.

Default Rate — Multi-Index Comparison

PIK Usage & Shadow Default Rate Trend

Spread Compression

Global Private Credit AUM — Historical & Projected

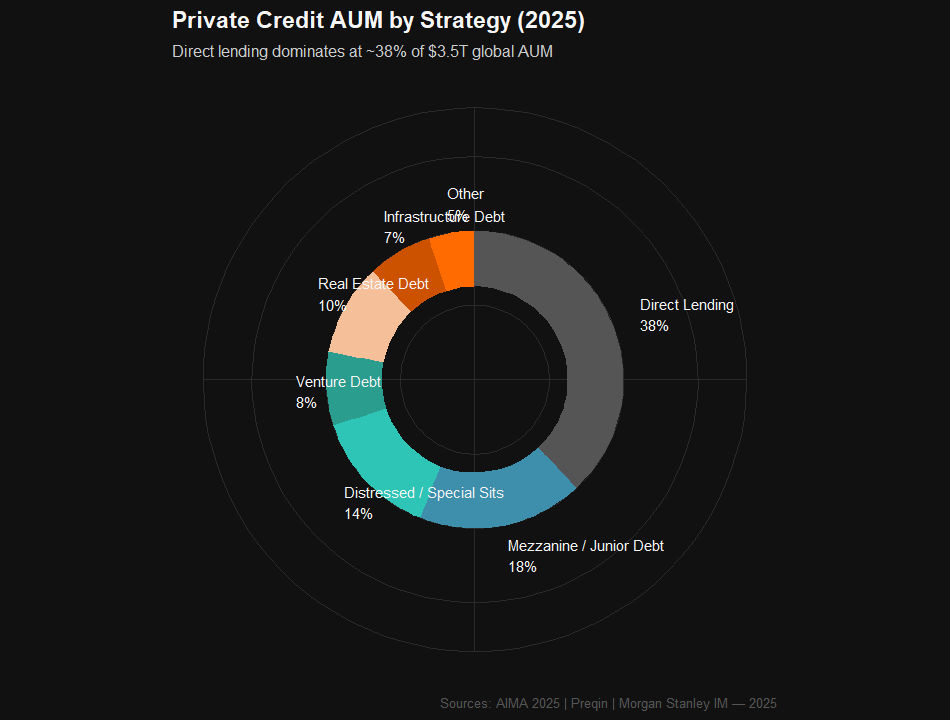

AUM by Strategy (2025)

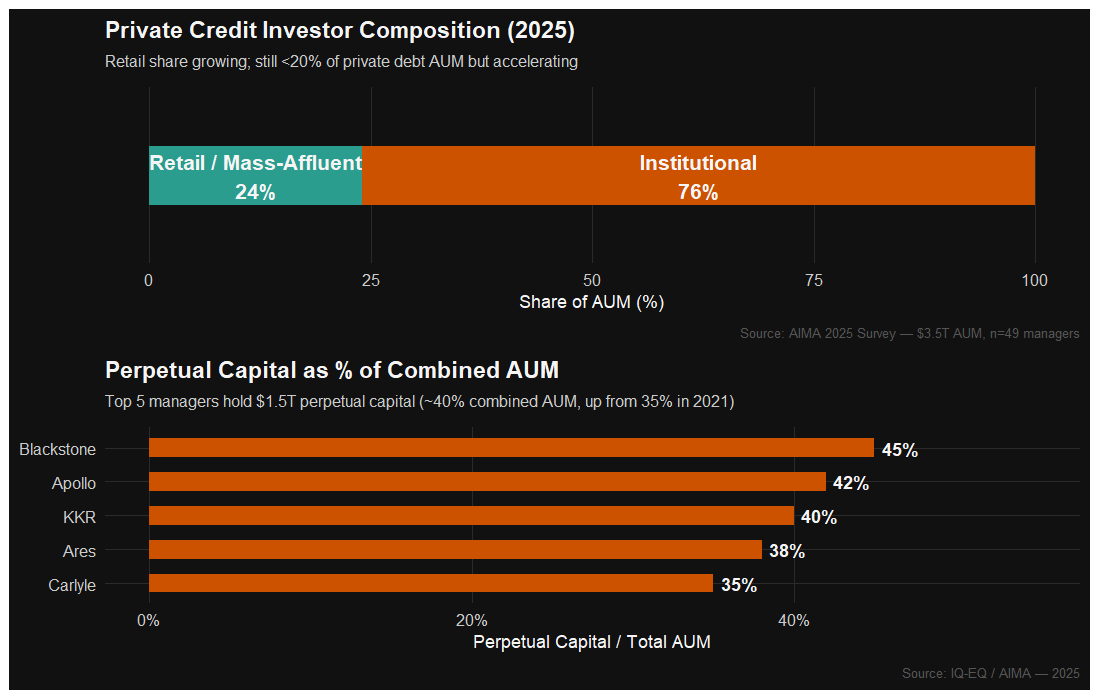

Investor Base Composition

Credit Secondaries Market — Record Volume

CLO Formation — BSL vs. Middle-Market

Summary Dashboard