Vol. 5 — Liquidity & Redemption Architecture

The Structural Fault Lines of Private Credit Liquidity

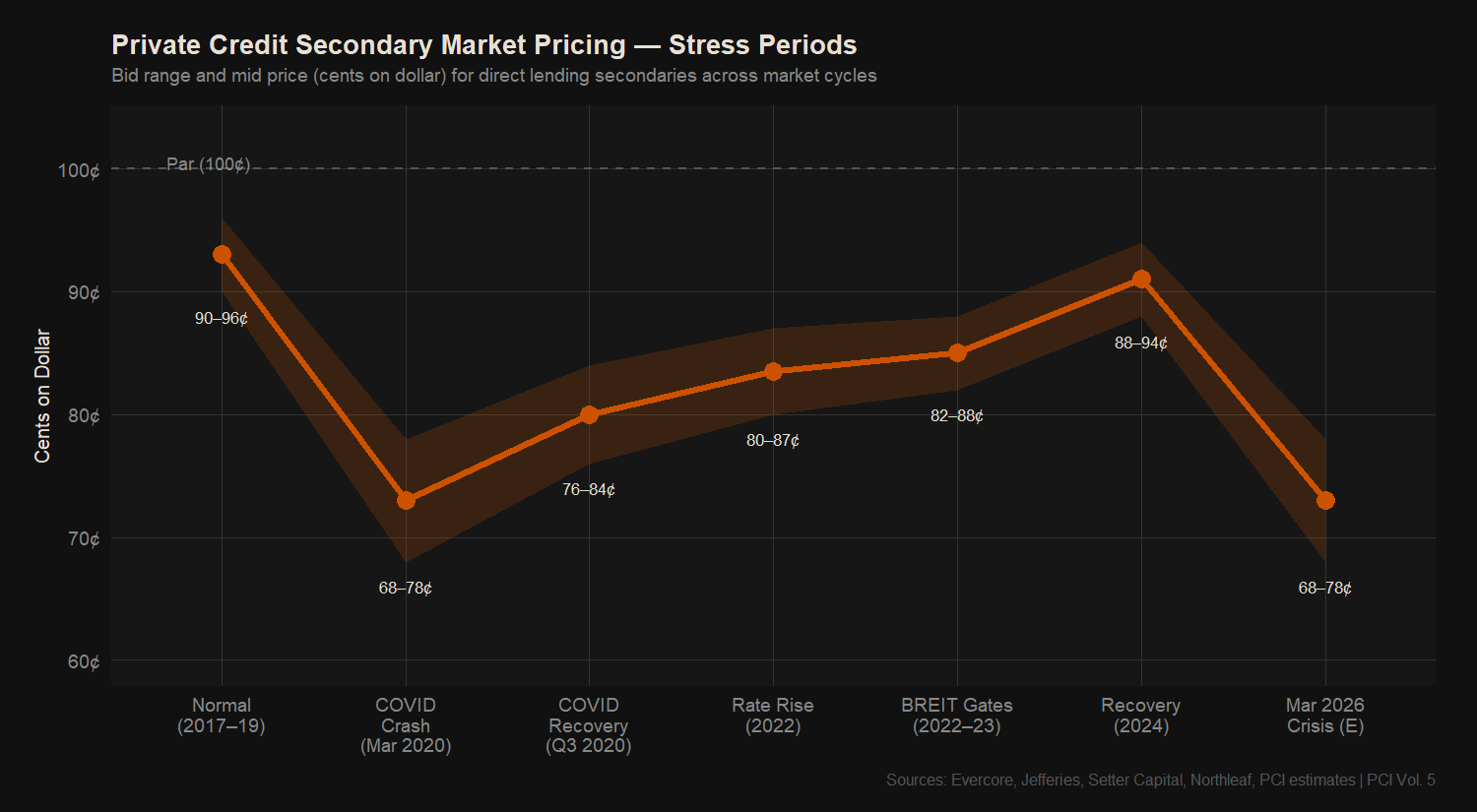

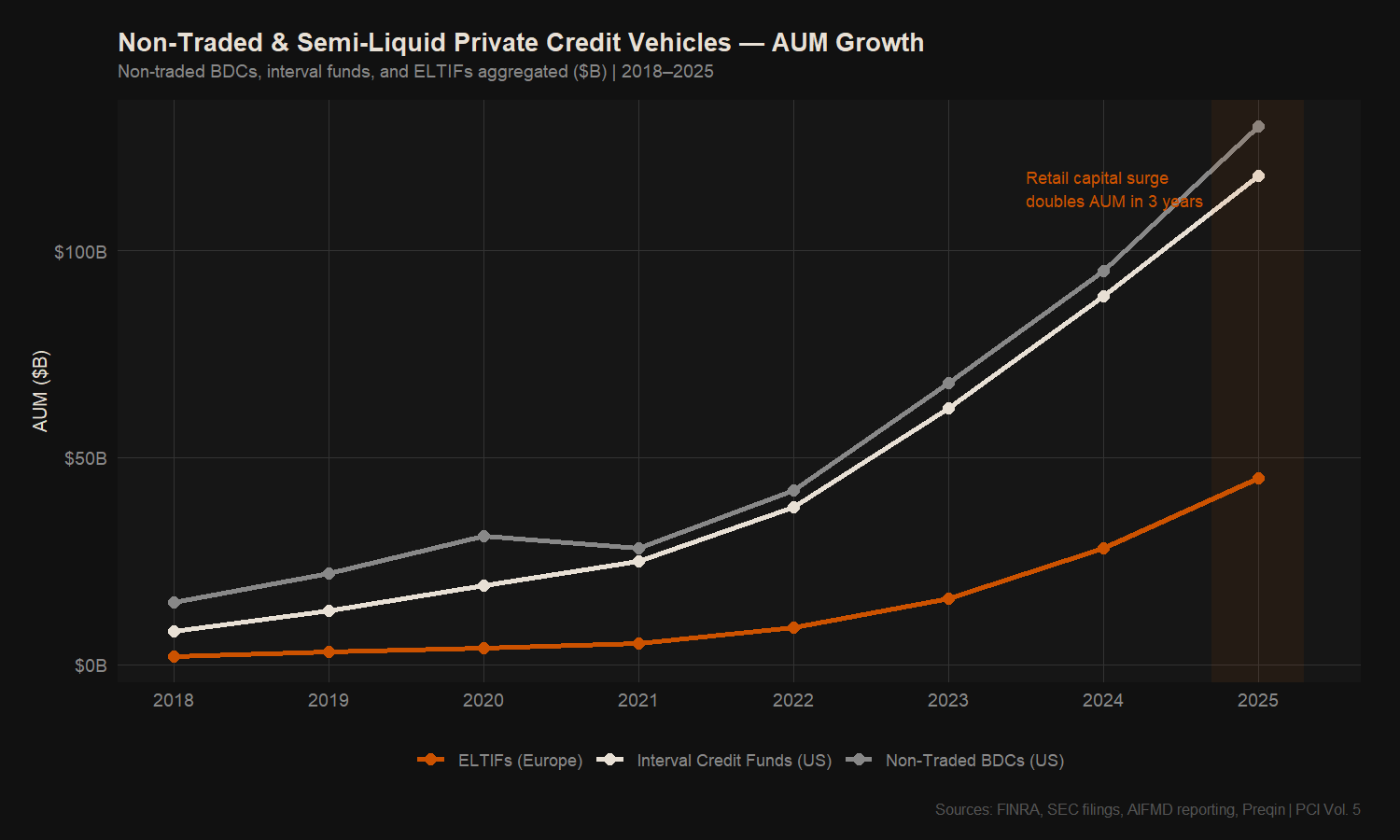

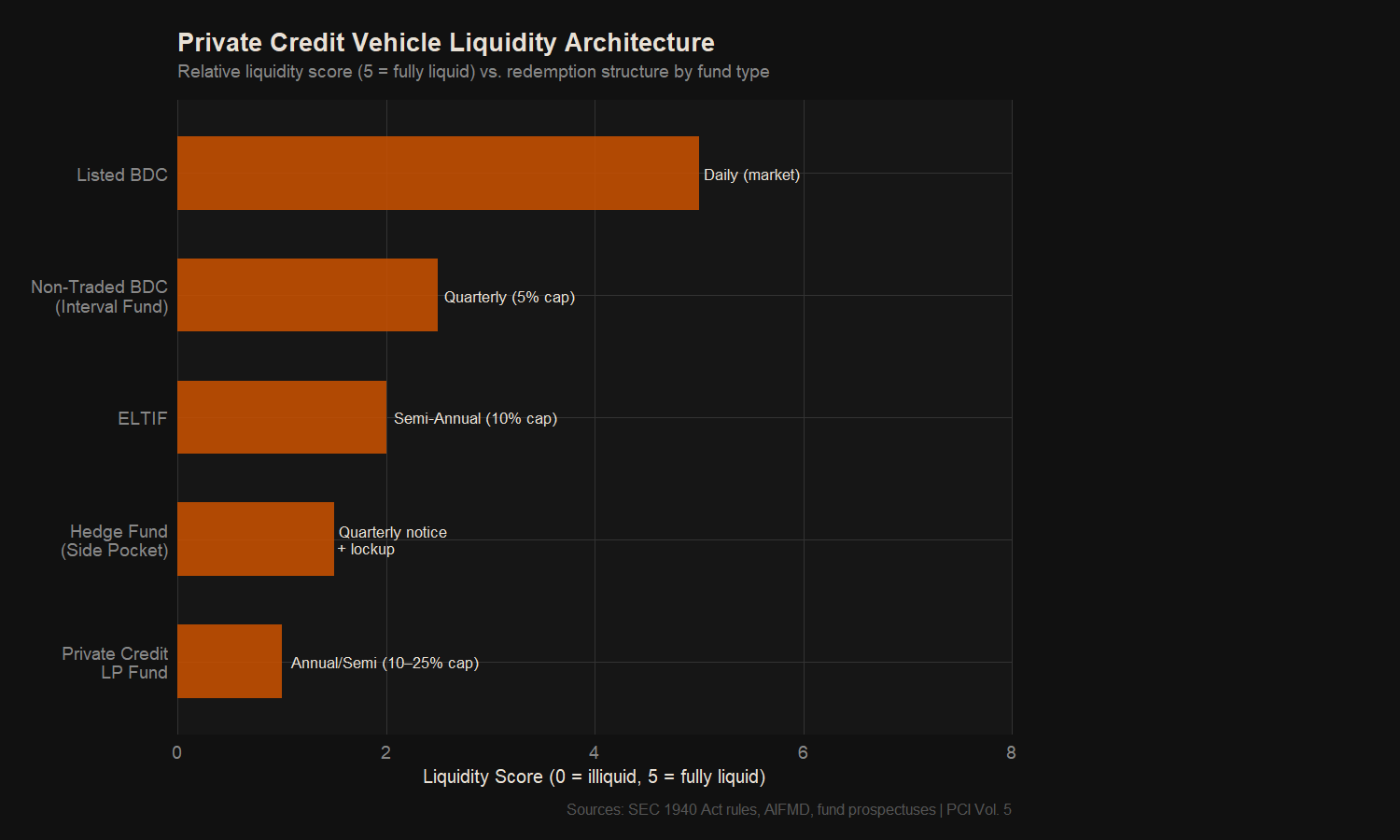

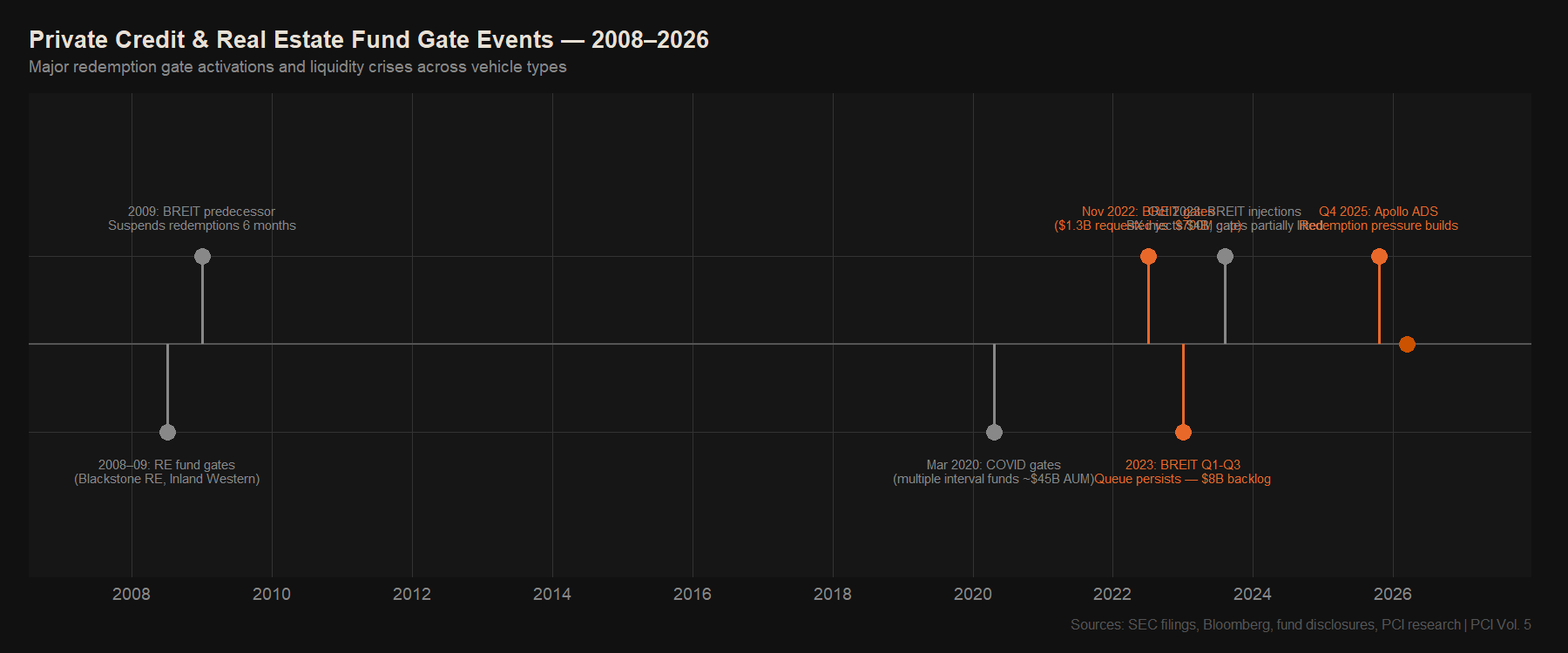

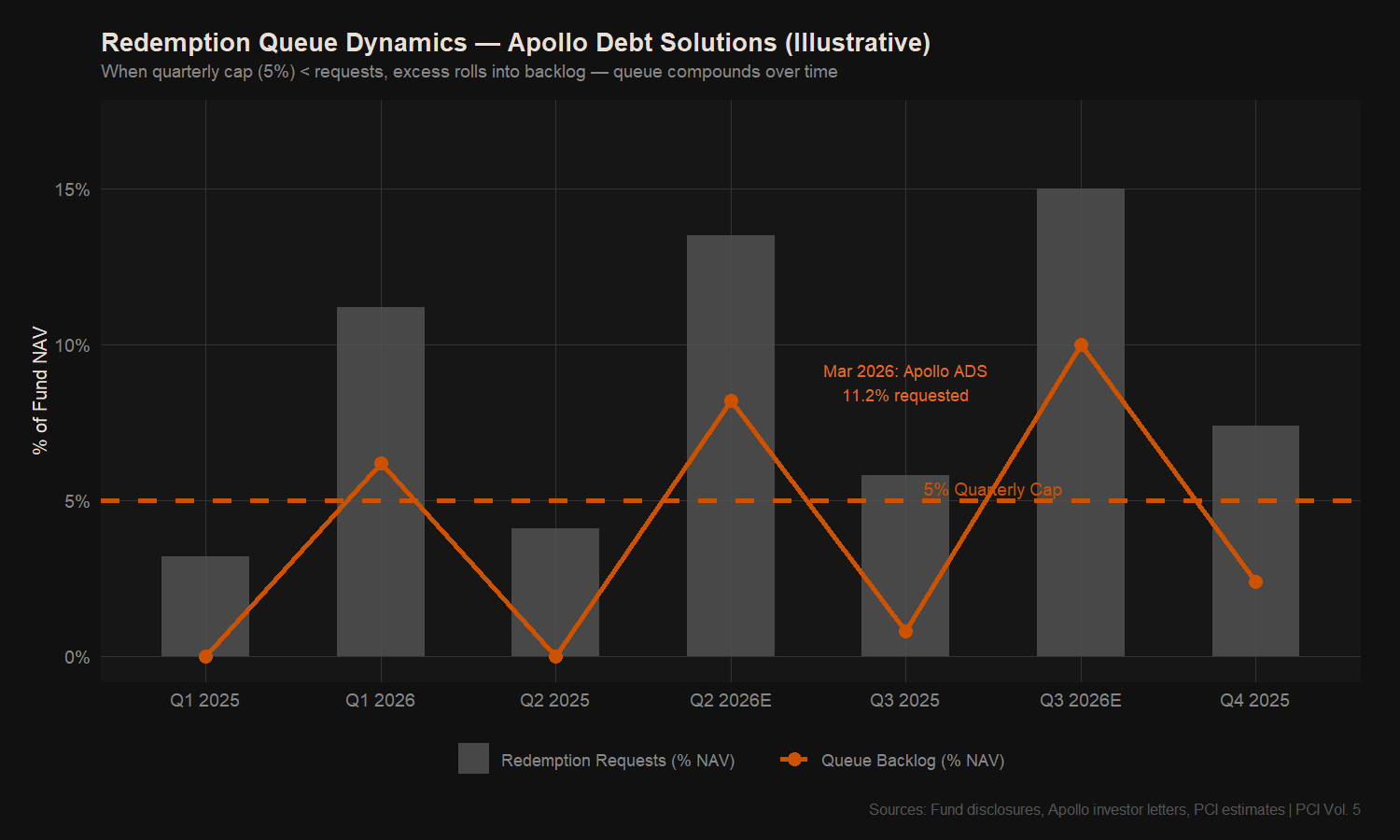

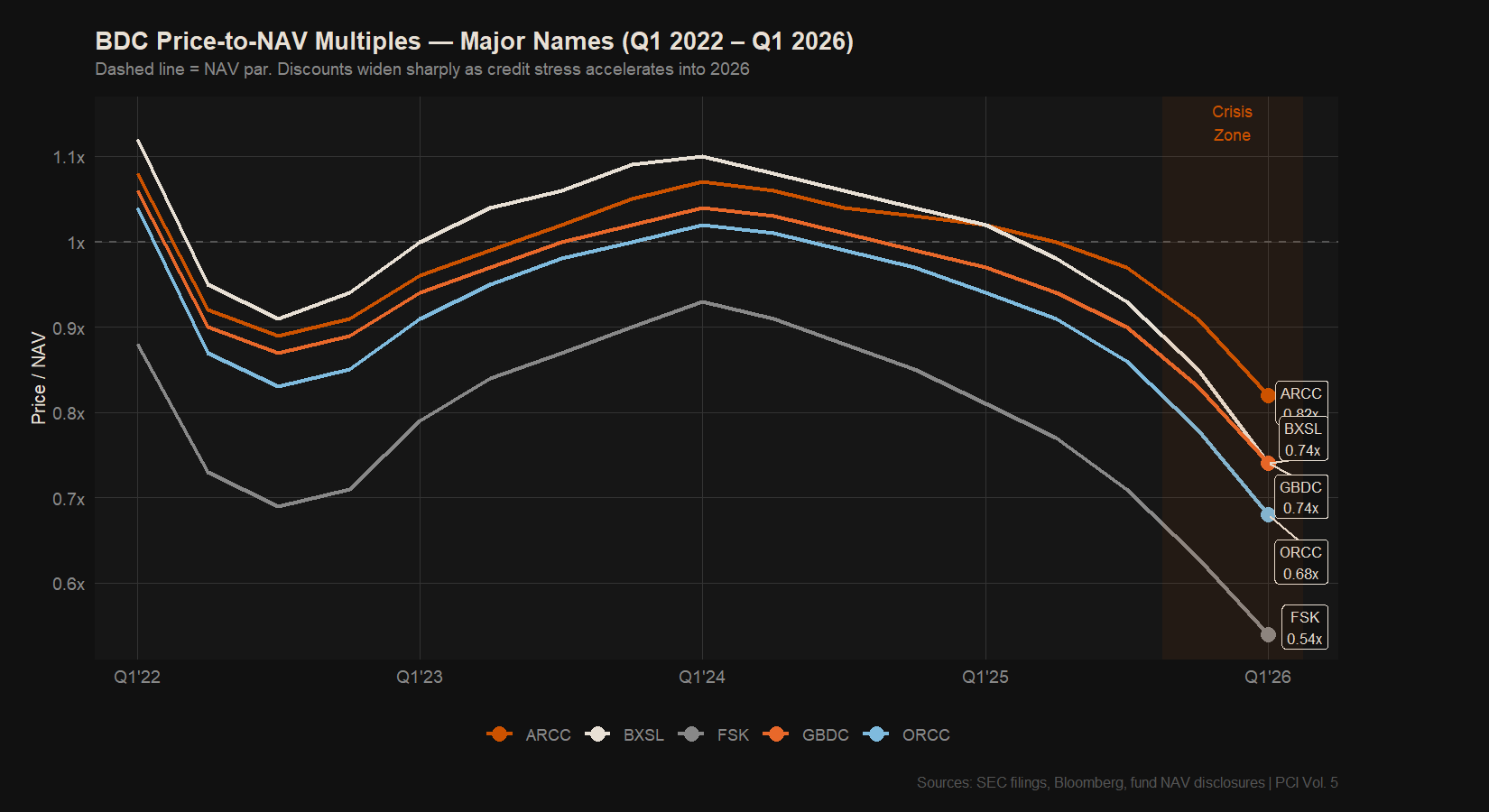

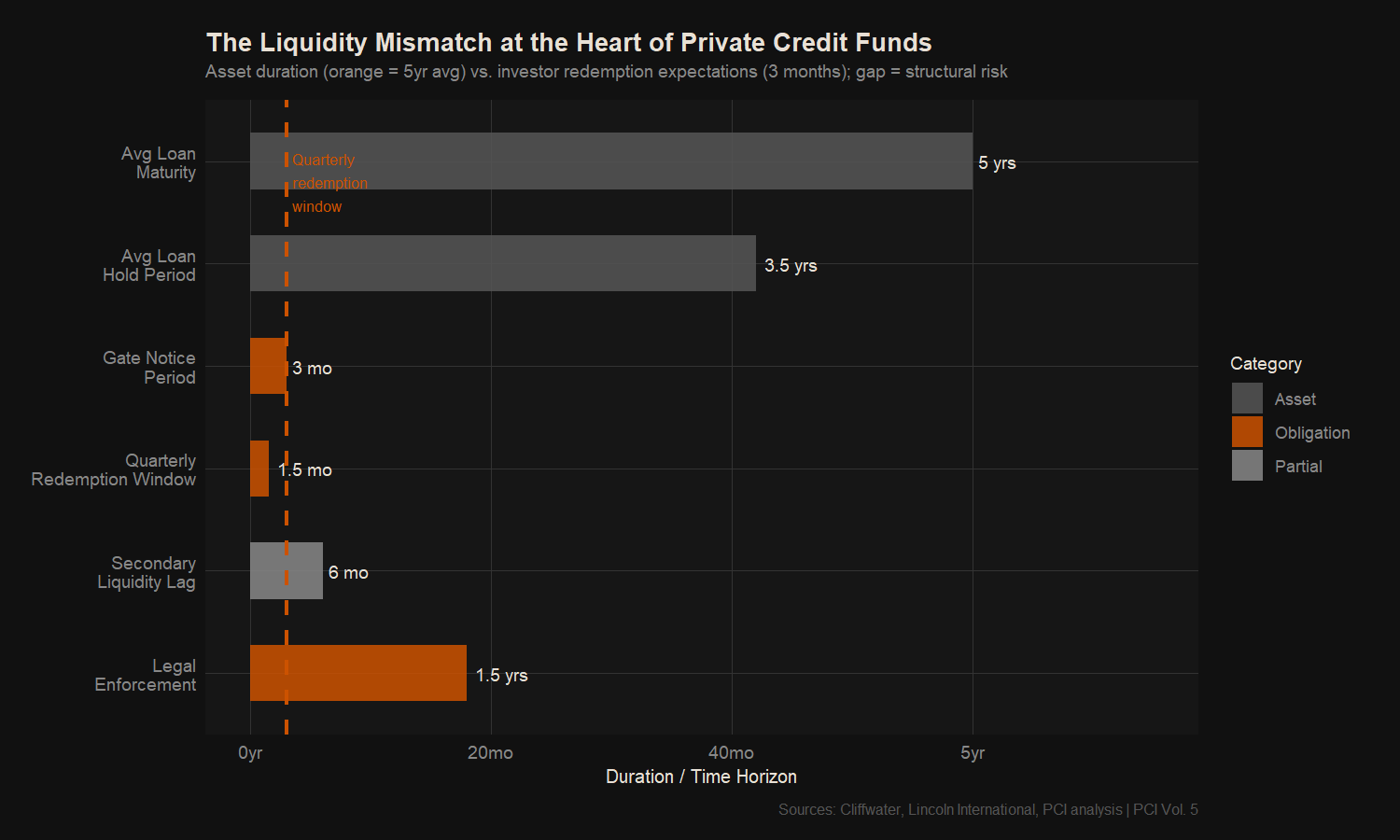

Non-traded BDCs, interval credit funds, and ELTIFs have grown from ~$25B (2018) to over $293B (2025) — an 11x surge driven almost entirely by retail wealth management distribution. These vehicles promise quarterly liquidity through a 5% gate cap, but in stress, redemption requests exceed the cap by 2x or more, creating compounding queues. Apollo ADS (11.2% requested) and Ares SIF (11.6% requested) triggered March 2026's triple gate event alongside Blackstone BCRED's $400M capital injection. The structural mismatch is simple: assets have a 5–7 year duration, windows are 90 days, and the 5% cap was designed for normal outflows — not a crisis. BDC P/NAV multiples have compressed to 0.54–0.82x; credit secondaries are pricing at 68–78 cents on the dollar.

Non-Traded & Semi-Liquid Private Credit Vehicles — AUM Growth (2018–2025)

Private Credit Vehicle Liquidity Architecture

Historical Gate Event Timeline (2008–2026)

Redemption Queue Dynamics — Apollo Debt Solutions (Illustrative)

The Liquidity Mismatch at the Heart of Private Credit Funds

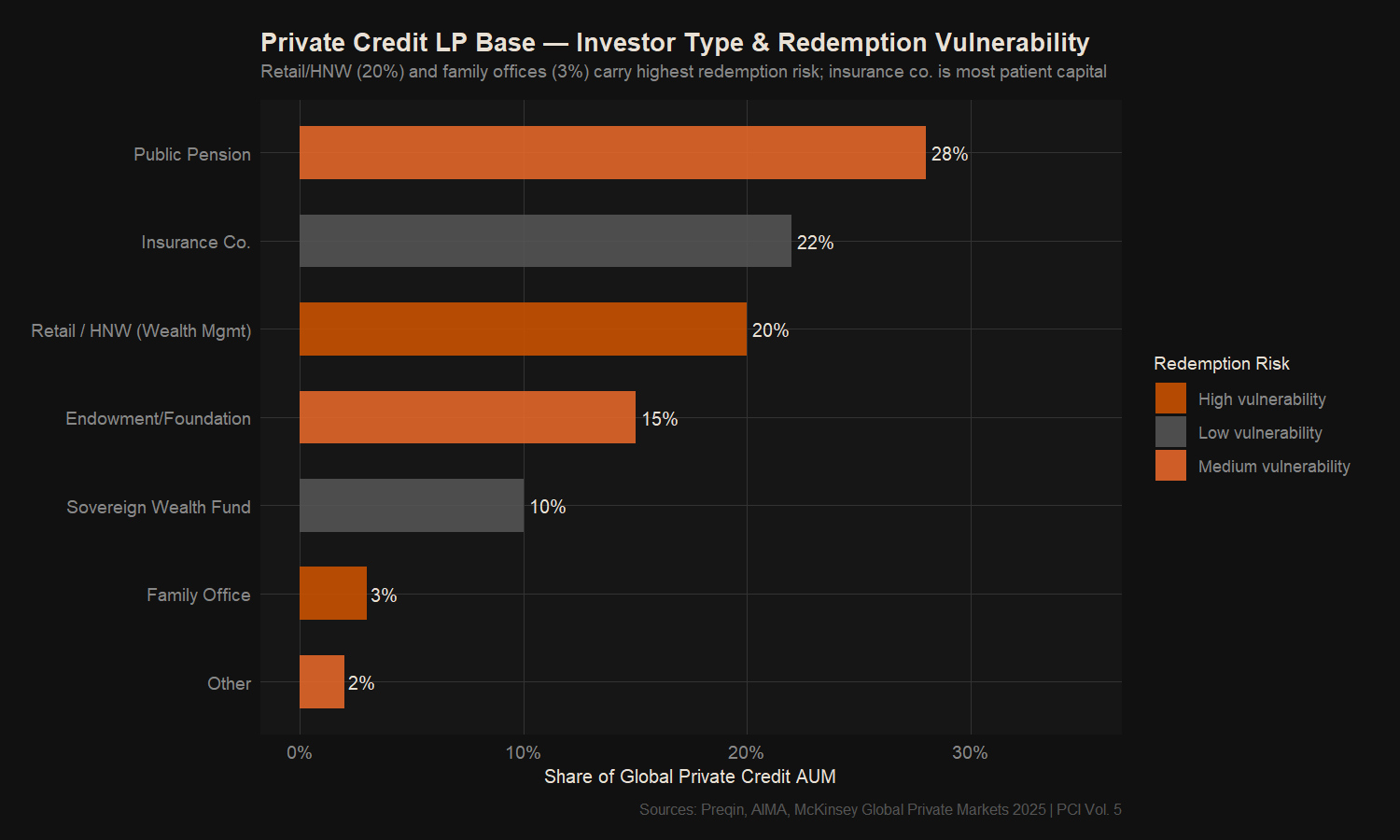

Investor Base & Redemption Vulnerability

Secondary Market Pricing During Stress Periods