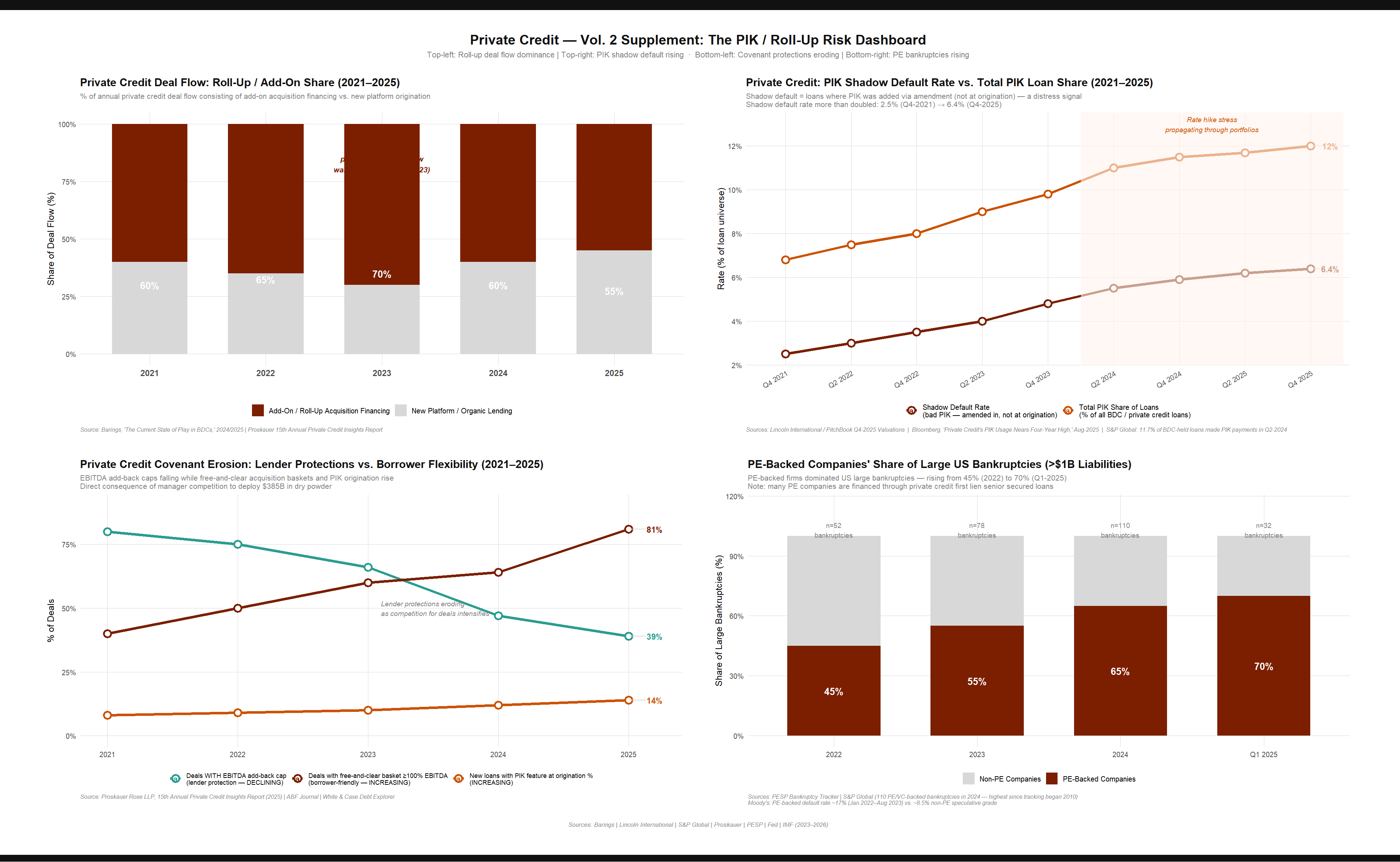

Vol. 2 Supplement — PIK & Roll-Up Risk

The Disconnect: PIK, Inorganic Growth & Shadow Defaults

Thesis

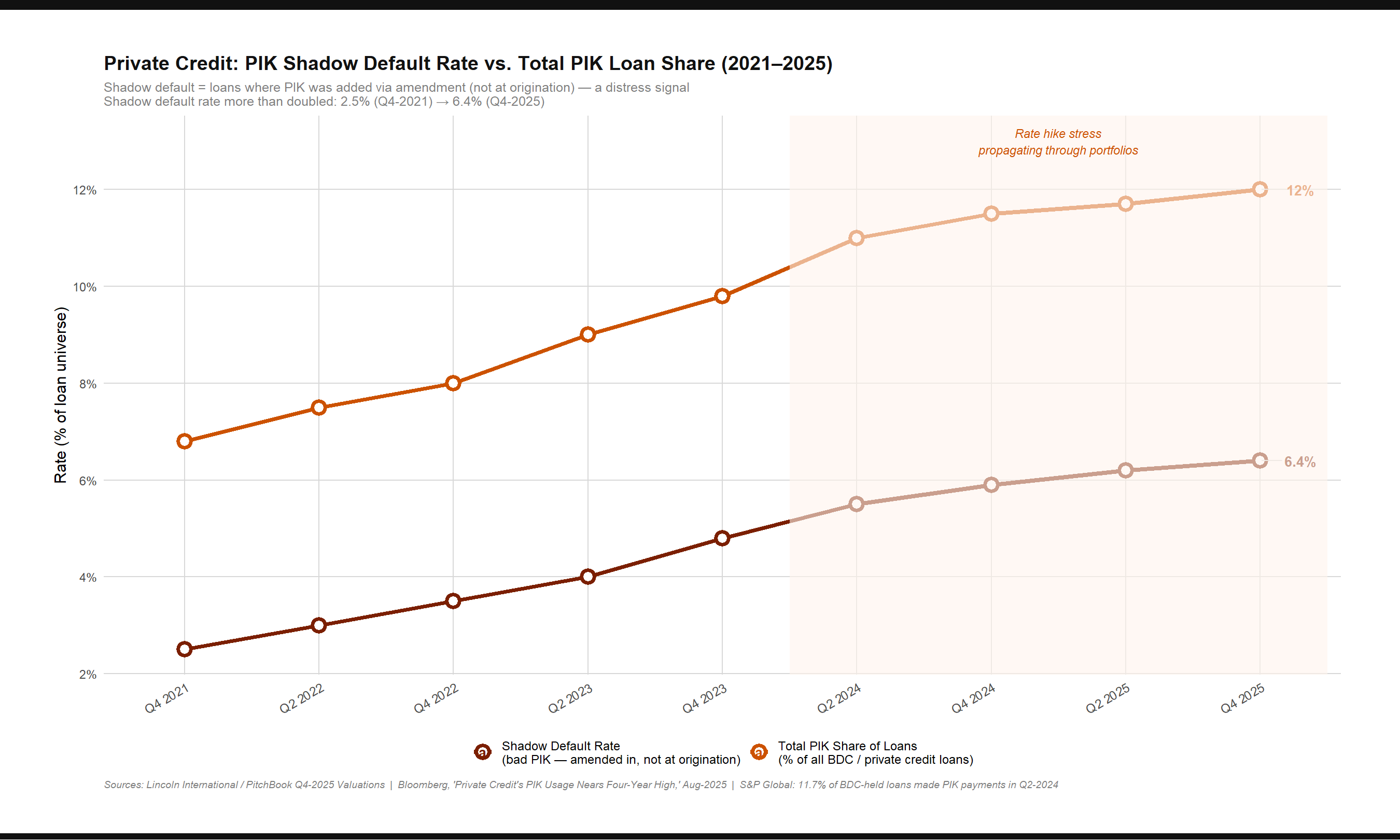

PIK interest added via credit agreement amendment — Lincoln International's "bad PIK" — functions as a shadow default signal. At 6.4% of par as of Q4 2025, it has more than doubled since Q4 2021. When combined with covenant-lite structures and inflated EBITDA add-backs, lenders are systematically underreporting stress in their portfolios.

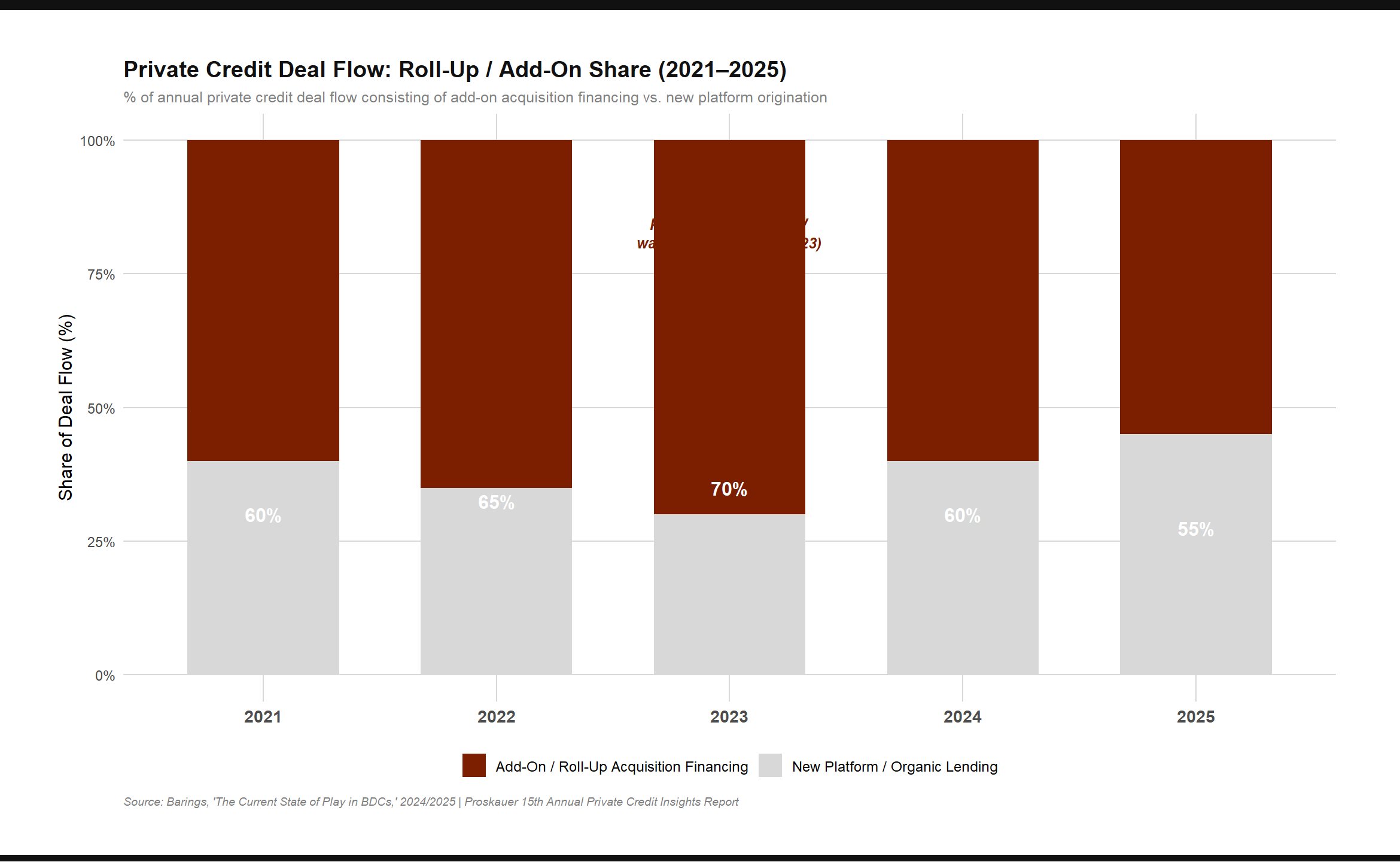

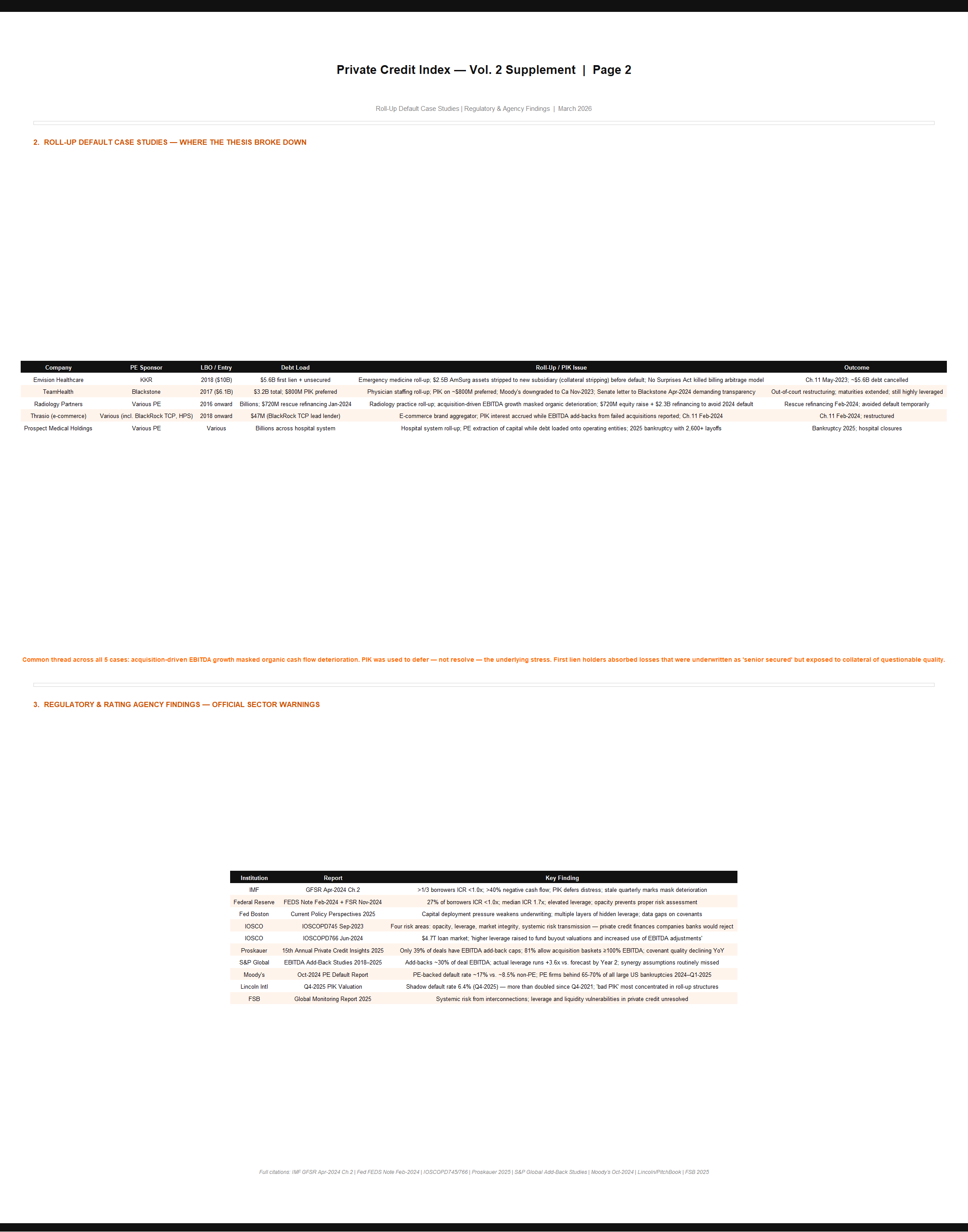

Roll-Up Deal Flow & PIK Shadow Default

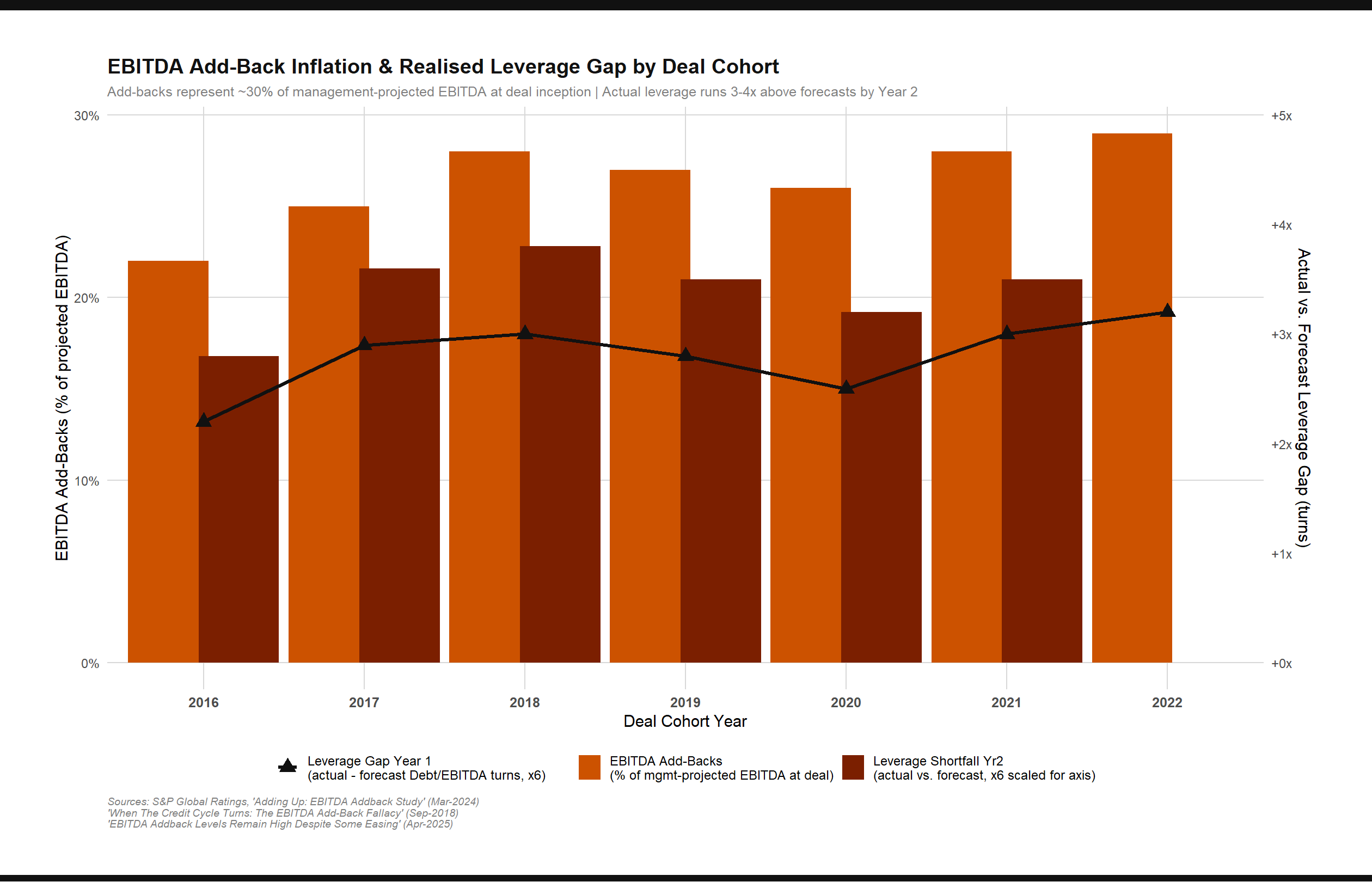

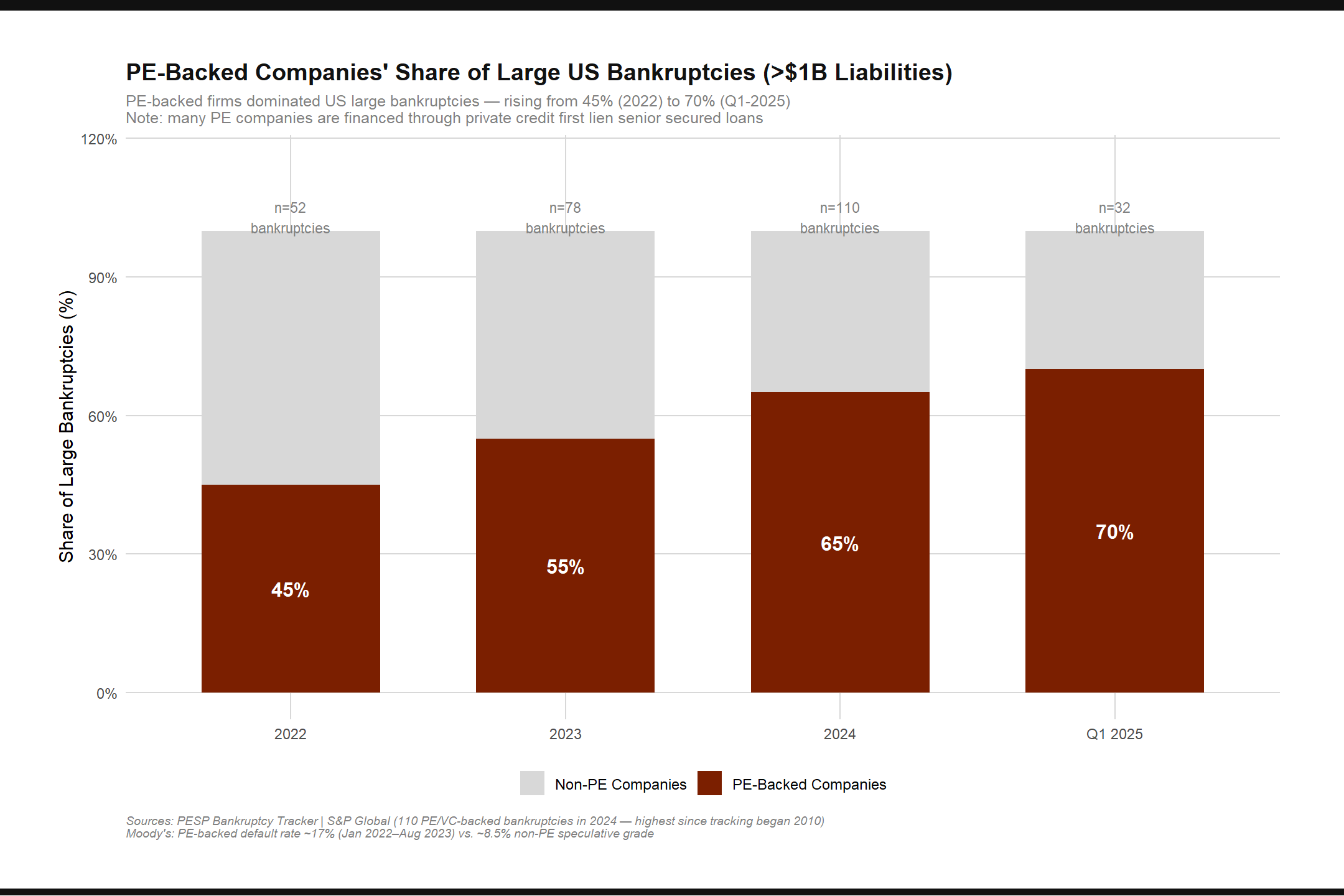

EBITDA Add-Backs & PE Bankruptcies

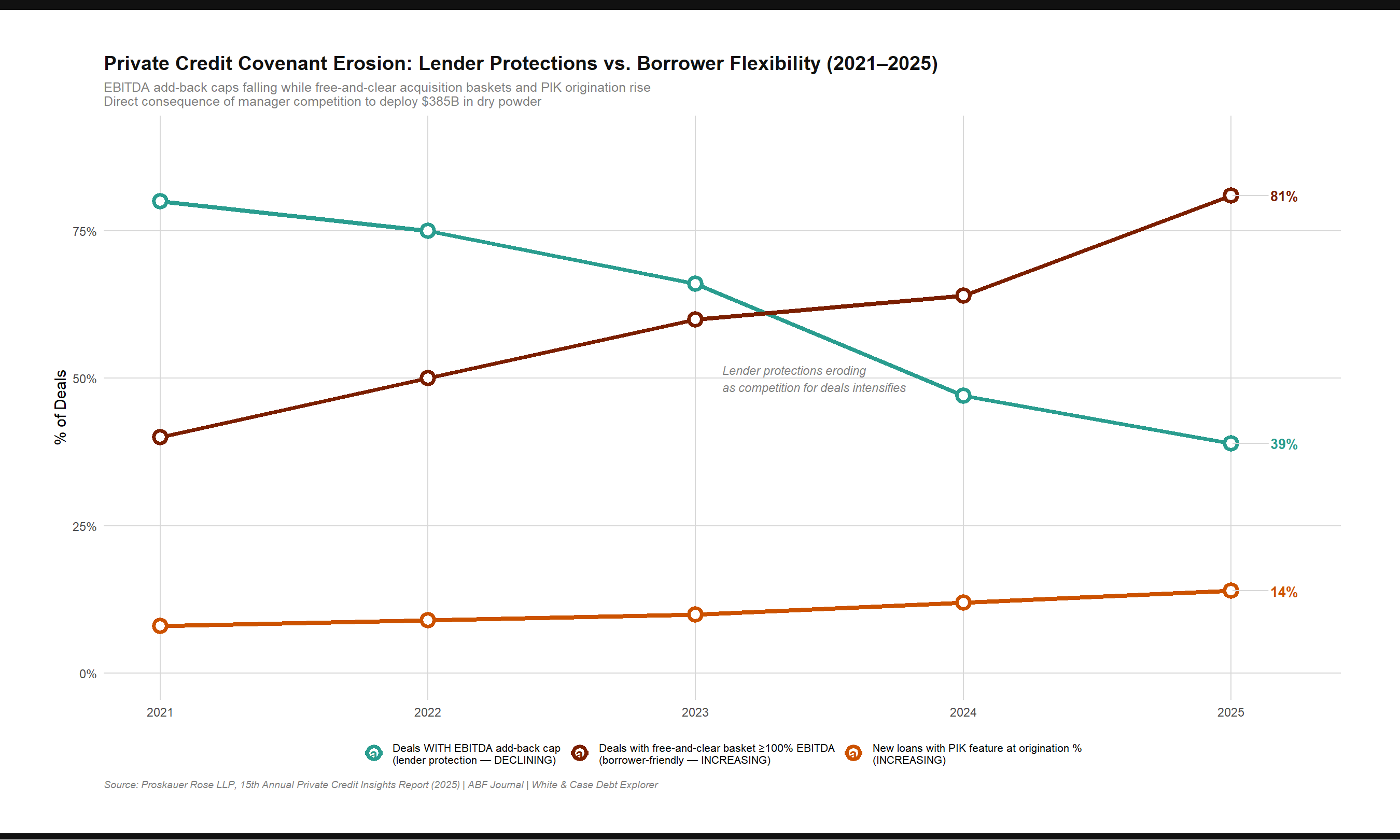

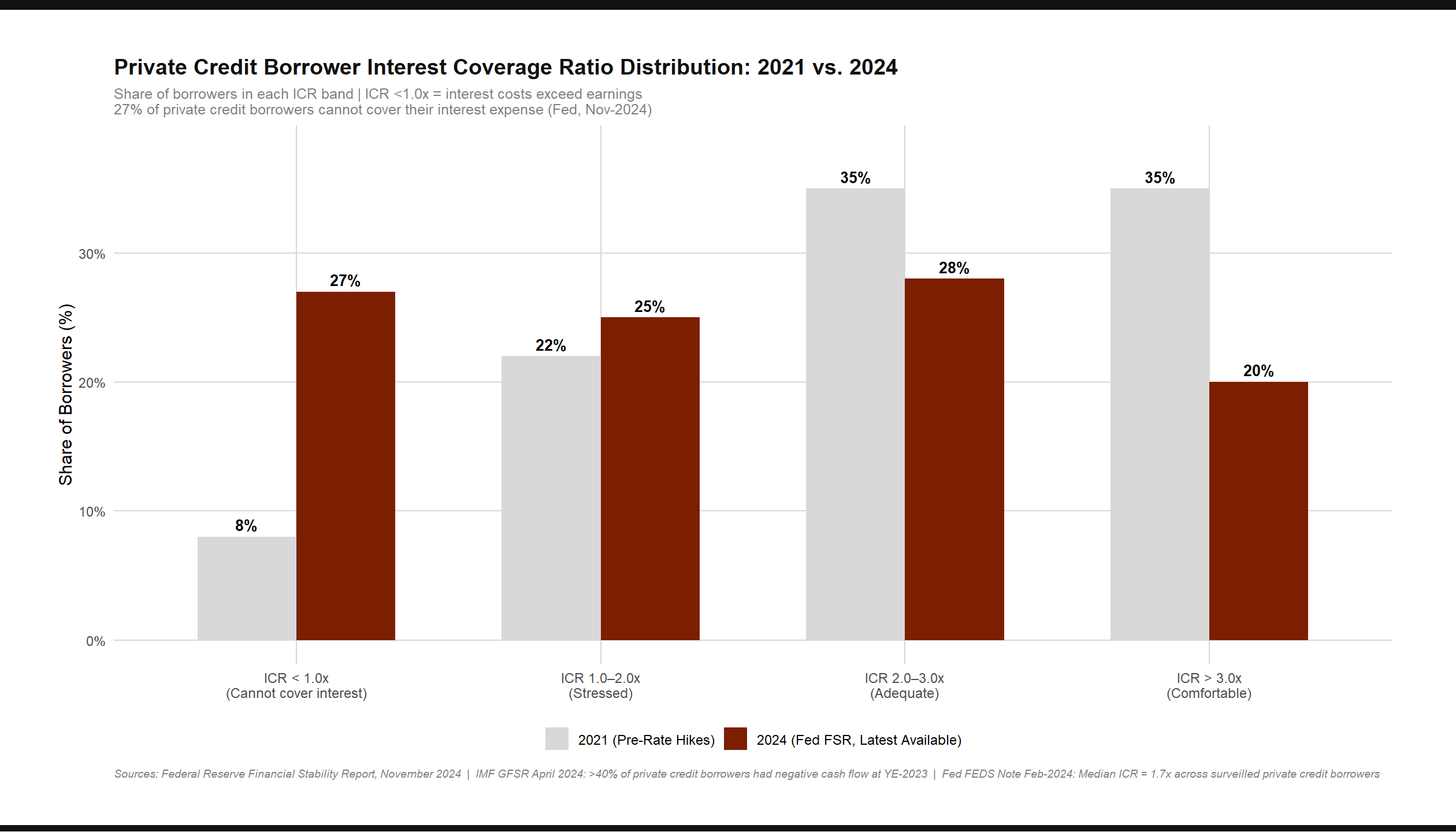

Covenant Erosion & ICR Distribution

Index Tables & Case Studies

Dashboard